Overview of my thesis about what is wrong about the direction of our politics

My blog interprets recent American history using Peter Turchin’s concept of the secular cycle. I call it America in Crisis because we are in the crisis period of this cycle. The secular cycle in industrialized nations is most readily tracked though economic inequality, or what Turchin calls popular immiseration. In his book Ultrasociety Turchin discusses cultural evolution as an important cause of historical change. I use a cultural evolution math model to explain the oscillations in economic inequality that define the American secular cycle since 1913. Inequality is used as a proxy for business culture, which is seen as a mixture of two archetypes. The shareholder primacy (SP) culture archetype is associated with high inequality. Low inequality is associated with the stakeholder capitalism (SC) archetype. Overall business culture is considered as a mix of these two archetypes, with the relative amounts of each determined by the level of economic inequality.

Inequality, cultural evolution, the wealth pump, and financial crisis.

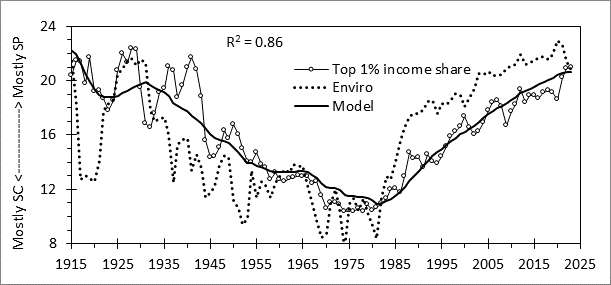

This figure shows how inequality has changed over time and the fit achieved with the cultural evolution model. Shown as the dotted line is the environment that selected for one or the other kind of culture. The environment is a linear function of top tax rate, interest rate and a measure of labor power (strike frequency as a percent of the maximum):

{kind=link}

1) Environment = 28.1 - 0.087*Labor Power - 0.083*Tax Rate - 0.79*Interest rate

The environmental effect is expressed as the level of inequality consistent with the present level of labor power, top tax rate, and interest rate. Given the environment, the present business culture (inequality) is simply a blend of the value called for by the current environment and its level in the previous year:

2) Inequality = 0.92*Inequality last year + 0.08*Environment

The small value of the environment coefficient shows how cultural evolution is slow. Attempting to change business culture/inequality through policy changes has a “half-life” of about 8 years. Following change in environment associated with a step change in inequality, it should take 8 years for the resulting evolutionary change to be half complete and 16 years for it to be three-quarters complete.

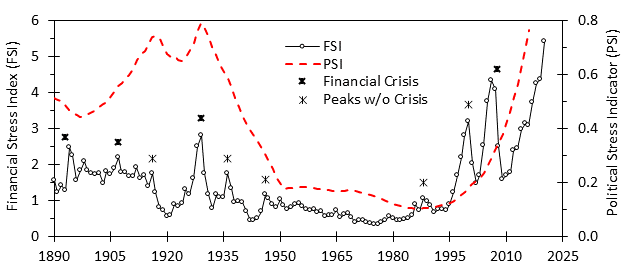

Turchin describes the processes leading to rising inequality as the wealth pump. In the American context the wealth pump can be thought of as an actual financial flow out of the real economy into the stock market where it contributes to rising market capitalization and potential financial crisis. Shifting from SC to SP culture cranks up the wealth pump, transferring income from the productive classes to the rentier classes producing both popular immiseration and an increased propensity for financial crisis that I measure using the financial stress indicator (FSI).

FSI is the product of two factors: speculative proclivity and market crash potential (MCP), which respectively represent speculative and Ponzi finance in Hyman Minski’s Financial Instability Hypothesis. Speculative proclivity is proxied by inequality relative to its long-term average value, while MCP is based on asset valuations. It is defined as the greater of stock market or real estate valuation relative to its long-term average. A plot of FSI is shown here.

{kind=link}

Inequality, elite overproduction, political stress and crisis resolution.

According the Turchin’s SDT theory describing the dynamics of secular cycles, inequality leads to a rise in the number of elites relative to the population, or what Turchin calls elite overproduction. Increased elite numbers and higher inequality both feed into rising political stress, as proxied by the political stress indicator (PSI). It is related to polarization, which can be thought of as a leading indicator of future political instability. We have had polarization for a long time, and it has since intensified into escalating political warfare. Political warfare can intensify into authoritarian policy or a breakdown in public order. See here for a discussion of past secular cycle crisis resolutions.

{kind=link}

The progress of the most recent complete American secular cycle can be summarized stepwise as follows:

1. Inequality rising under SP culture during the stagnation period (1893-1907)

2. Development of a stock market bubble via the wealth pump during the crisis period (1907-29).

3. Growing bubble implies growth of speculative and Ponzi finance as captured in the FSI.

4. Collapse of bubble leads to financial crisis.

5. If PSI is low, the political dispensation survives (1907, 2008).

6. If PSI is high, political dispensation is discredited. Crisis period ends and resolution period (1929-1942) begins

7. New regime shuts down wealth pump and enacts policy to shift from SP to SC culture

8. The shift from SP to SC becomes locked in with the confirmation of FDR dispensation (1940)

9. New secular cycle begins with a growth period (1942-1978).

10. Policy under the FDR dispensation causes SC culture to displace SP, as manifested by falling inequality.

11. Wealth pump remains inoperative, making financial crisis impossible.

12. Inequality bottoms in 1978 and then begins a rising trend, Growth period ends and stagnation period (1978-2006) begins.

13. FDR dispensation replaced with that of Reagan (1980). Wealth pump reactivated.

14. Neoliberalism (defined as policy promoting SP culture) is a mainstay of the Reagan dispensation.

15. SP culture becomes dominant as inequality steadily rises.

16. Congress reauthorizes financial crisis1 over 1997-2003.

17. Elite overproduction leads to polarization in the 1990’s and 2000’s and political warfare in the 2010’s and 2020’s. Return to 1.

How the secular cycle plays into our politics

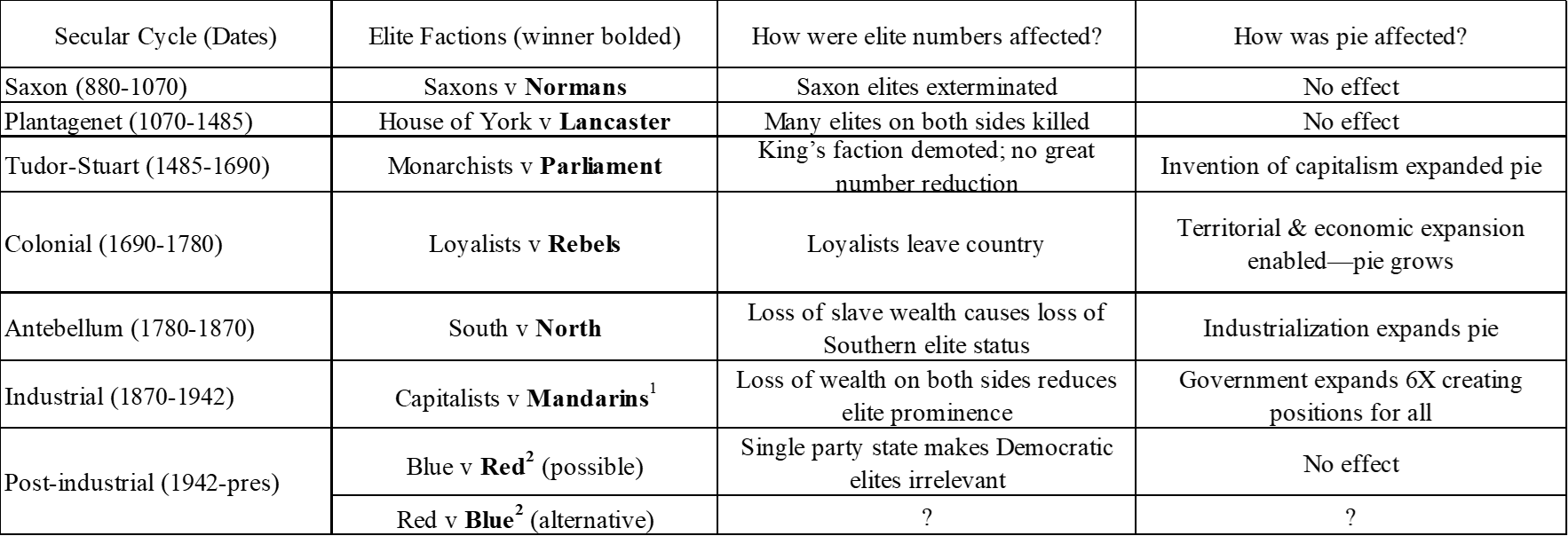

If Turchin’s ideas about secular cycles are correct, the present crisis era will be resolved at some point in time. Resolution removes the cause of the crisis, which is an excess number of elites relative to the “size of the pie” (available elite positions). This can be done by reduction in elite number, increases in the size of the pie, or both. This figure outlines how the six previous Anglo-American crises were resolved. Most of these resolutions have been brutal, involving killing of elites, economic ruin or exile of the losing faction, or some sort of civil war. A plausible case can be made that President Trump will attempt to establish a MAGA dynasty as a way of resolving the present crisis. This might he done using the Republican party as a vehicle using fixed elections, perhaps with JDVance as Trump’s hand-picked successor, or through an unforeseen mechanism such as Elon Musk forming his own party and conducting an unfriendly acquisition of the MAGA-Republican brand, forcing Trump to accept Musk as his successor.

{kind=link}

My own guess is the American political system will continue. Here President Trump’s actions are interpretated as his efforts to restructure the aging Reagan dispensation into a new Trump dispensation, like McKinley and Roosevelt restructured the Lincoln dispensation to grant their party another 36 years of political dominance. According to Stephen Skowronek’s Political Time model, a dispensation is a period of political dominance by one party. Franklin Roosevelt established his dispensation (1932-79) through his New Deal, which created a very favorable economy for the working and middle classes, while Reagan established his dispensation (1980-present) as a reaction against the New Deal that I call Neoliberalism. Dispensations age, after which voters can come to despise both parties, trading off between them every other term as happened over 1880-92 and 2012-24.

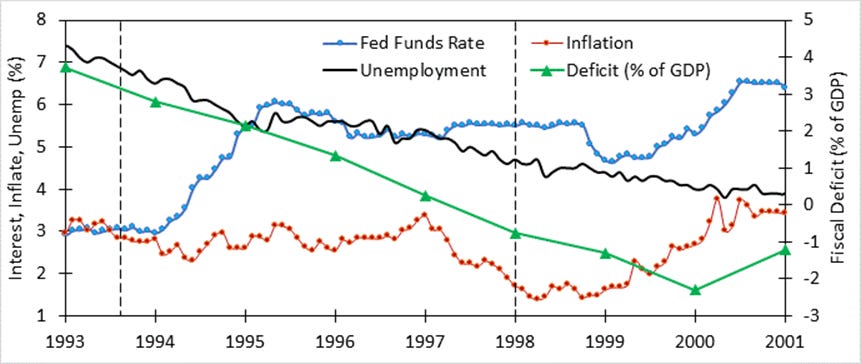

Whereas MAGA seems to be playing the normal role of one of the elite factions in a secular cycle crisis resolution showdown, their Democratic opposition seems asleep at the switch, completely unaware of what is going on. I have long pondered why Democrats do not press their advantages when they get them, as Republicans do. For example, President Clinton had run, and won, on a slogan “It’s the economy, stupid.” I recall the beginning of the new Clinton administration featured “gays in the military,” rather than the announcement a new economic program. This was followed by the formation of a task force to develop a national health program, a long-time Democratic policy objective, but not the new approach to the economy the campaign slogan implied. They followed the next month with major tax reform, passed in August 1993 (see dashed line in Figure 1) which significantly increased revenues leading to falling deficit.

The hope was that Fed Chairman Greenspan would lower interest rates in response to lower deficits expected from the tax increases. He raised them instead in 1994. Inflation was unchanged by the 300 basic point interest rate hike, averaging 2.9% over the year before the hike and 2.8% in the year after. The hike stalled rising employment for a year and a half, slowing the increases in working-class wages the campaign had promised. It was only after a capital gains tax cut passed by the Republican Congress took effect in 1998 (see dashed line in Figure 1), after which the stock market went parabolic, that the Fed cut rates in response to a sharp 22% decline in the market. Six months later the Fed began a 175-point sequence of hikes to deal with rising inflation.

Figure 1. Inflation, interest rate, unemployment rates and deficit spending over the Clinton administration

The Fed hiked rates to fight non-existent inflation after Clinton had begun a program of deficit reduction and only cut rates after a Republican tax cut supercharged a stock market bubble that was followed by a panicky correction in October 1998. Despite balancing the budget (something no Republican had done for forty years), passing a paid-for bill to put an additional 100,000 police officers on the job, achieving a 40% decline in the murder rate, voters elected a Republican who proposed to cut taxes and piss away the hard-won surplus. At the time I thought Clinton had made a mistake to focus in getting the fiscal house in order in order to be rewarded by a Fed chief who was a former Ayn Rand acolyte. I did not know then about the Skowronek political cycle and dispensations. As I now know, there was nothing the Democrats could have done. As the first preemptive president, Clinton’s ability to act was constrained by the Reagan dispensation, much as Eisenhower had been by the Roosevelt dispensation. Eisenhower had resisted Republican calls to cut taxes; instead he kept taxes high, ran balanced budgets, and ended an unpopular war. Despite his successful presidency, he, like Clinton, was succeeded by a opposition party president who cut taxes and ran deficits, wrecking the economy.

How the dispensation hems in Democrats

With this new understanding, Clinton is absolved; there was nothing he could have done to change things, he was a prisoner of the political cycle. But what about Obama? Obama was the second preemptive president, making him like Nixon-Ford in the previous cycle. Nixon had inherited an unpopular war, a booming economy, a budget surplus due to a temporary tax surcharge, and a Congress controlled by the opposition, conditions ill-suited for major policy change. Obama’s hand was much stronger. He had inherited two unpopular wars, an economy in collapse, a soaring deficit, and a had a Congress controlled by his party. The fact is, Obama and the Democrats in 2008 did not press their advantage the way Republicans do, or the way Franklin Roosevelt did.

Financial crisis arose following the bankruptcy of Lehman Brothers in September 2008, before the election. The issue at hand was a bill formulated by the Bush administration that was intended to stem the crisis in its early stages as J.P. Morgan had done a century earlier. This plutocrat-friendly TARP bill was rejected by Republican congressmen 63-37% and only passed with a lot of Democratic votes. A Democratic presidential candidate playing hardball would insist that politically unpopular action to address a crisis that happened on the Republican watch should see Republicans voting for their own rescue plan. Democrats could have pledged 65 votes and leave it to the Republicans to whip the 153 votes needed to pass from their own 171 member caucus.

After losing the 1932 election, President Hoover made numerous efforts to craft a bipartisan policy to address the Depression. Hoover was particularly concerned about Roosevelt’s “New Deal” which he rightly feared would involve abandoning the gold standard. Roosevelt did not take him up on his offers. Had Obama persuaded Democrats to play hardball with Bush in 2008, he could have done what Roosevelt did with Hoover, let the blame for the mess Republicans had created fall cleanly on the Republicans.

Obama did not do this, because he believed (as I also did) that if Democrats demonstrate that they know what they are doing and govern better than the incompetent Republicans, voters would figure this out and vote for them out of simple self-interest. The 2010 election showed this was not the case. Politics shifted away from “real things” like the economy and war/peace issues to culture war stuff like the Tea Party Movement and Birther conspiracy. Culture war politics are largely symbolic for which the Republican-favoring Reagan dispensation governs. With their TARP decision, Obama and the Democrats were as boxed in as Clinton or Eisenhower had been.

Creating a new dispensation requires luck or bold action

As I discussed in my dispensation article, two of the four most recent dispensations arose by luck, extraneous factors gave Reagan and McKinley their dispensations. Lincoln created his dispensation by prevailing in the Civil War, and Roosevelt his by creating a sharp improvement in working class lives that Roosevelt made sure was associated with him in voters’ minds. Trump’s efforts at dispensation building lack nothing for boldness, but they are unlikely to deliver the change promised. Democrats thus far have shown no understanding of these issues or at least have made no moves suggesting an awareness of the need for a new dispensation. The time is limited. The infrastructure and judicial precedents for a transition to authoritarian rule is being laid down now. Failing to achieve a crisis resolution through a dispensation change as Roosevelt did, Republicans appear to be setting up a back-up plan for elimination of democracy altogether as Germany did last cycle.

Assuming our political system survives the present administration, and Republicans lose a Rule 1 election in 2028, they will very likely achieve the authoritarian transition after the next election. The alternative, it would seem, is to drift into civil war.

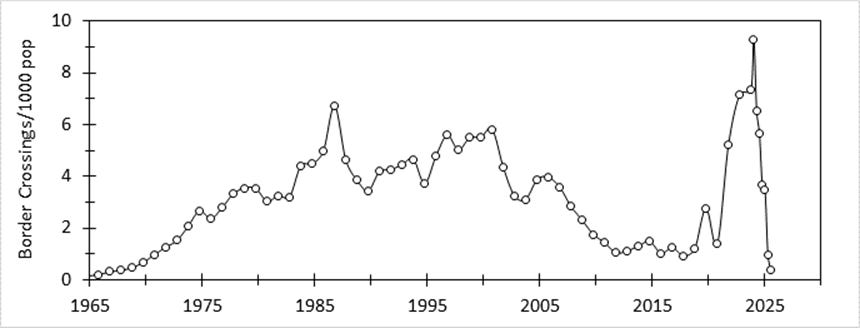

To prevent this Democrats must make preparations to pursue a new dispensation in what could be their last opportunity to do so. In a recent post, I suggested some things Democrats and the Left could do to make this task easier. One was to replace socialism with a return to a better kind of capitalism as the progressive take on economics. I take a stab at a Democratic economic vision here. The second thing was to remove the immigration issue from contention by simply accepting the current low rate of southern border crossings (see Figure 2) as standard Democratic policy going forward while condemning the Trump deportation program as cruel and economically idiotic. The issue of citizenship for illegal immigrants should wait until low levels of border crossings under both parties has come to be seen as the new normal. The thorny issue for such deals in the past had always been around control over the rate of immigration, solve this and a deal becomes possible.

Figure 2. Annual rate of southern border crossings relative to population

Finally I argued that Democrats need to distance themselves from the cultural progressives, as their views are a major liability. This need only be temporary; progressive cultural ideology has been radicalized by the current creedal passion period (CCP). The last CPP saw the days of rage, so the Great Awokening has nothing on that era in terms of radicalism. Nevertheless, it would be wise to wait under well after the CPP has ended (the math model forecasts this for 2027) to revisit these cultural issues.

I recall just after the Obergefell decision in 2015 when transgender issues began to rise into public consciousness, thinking it’s “gays in the military” all over again. But this time, rather than the issue settling down, it took off and became a big thing. This is the effect of the Great Awokening CPP. Gays in the military was associated with an uptick of “political correctness” (an earlier form of “wokeness”) and a “spiral of violence” involving right wing terrorist groups2 whose growth was suppressed because it was “out of cycle” (see the 1990’s uptick in instability in this figure). When trans issues (and other “woke” issues) showed up a couple of decades later they were “in cycle” and so they grew like topsy.

{kind=link}

If Democrats wish to remain relevant, it is imperative that they start thinking in terms of dispensations and secular cycle crises in order to become aware of dangerous territory our country will face over the next decade or two.

When researching historical stock market performance in the mid-1990’s I noted that the two major US crashes (1929, 1987) involved stock bubbles that began with reductions in capital gains tax rates to 20% or lower. At this time, I was pondering whether the post-1982 stock boom would end with a blow-off top and crash like in 1929 or dribble out as in 1966-68. In Dec 1996 Fed chairman Greenspan gave his famous “Irrational Exuberance” speech in which he suggested the market was fully valued. Six months later the market was 20% higher, flirting with bubble territory, when Congress passed a capital gains tax cut lowering the rate from 28% to 20%. Such a policy should encourage capital gains which come from higher prices. I called this law the “stock market bubble and crash act” on the day it was passed and now knew the bull market would end with a blowoff top as in 1929, and stayed invested until August 1999, after which I began writing my book on stock market cycles. And we got the bubble and crash: stocks rose 60% after the tax cut was passed before crashing down to 10% below from where they started. In 2003 Congress cut capital gains again in another bubble act. Since the hot asset class then was real estate, I called it the real estate bubble act. We got the bubble, but I did not expect a financial crisis.

The spiral began with the Ruby Ridge incident in 1992, followed by the Waco insurrection in 1993 and the Oklahoma City bombing (on the two-year anniversary of the end of the Waco siege) after which the cycle of violence fizzled out.

BTW...I'm not here to troll you. I got a lot out of your cycle theory books (and from others like Turchin, Friedman and Neil, Howe) back in the day and think these long cycles do provide a great framework to analyze markets and world events. That said, because the circumstances are different, the cycles are different. If we don't use them as precise predictors, but rather as guidelines, they are very useful in making sense of the world.

The "Wealth Pump" is particularly associated with periods after inflation spikes (Kondratiev falls). The Era of Good Feelings and the jacksonian era after the War of 1812 (real estate and cotton), The Gilded Age after the Civil War (railroads and steel), The Roaring Twenties after WWI (autos, utilities) and the current era (information technology) after the Vietnam and the Cold War. All the tools we developed after learning from previous crises (monetary policy, fiscal policy, elastic fiat currency, positive inflation targets) have been used to prevent depressions during this period, but have elongated the downwave. Thus wealth creation opportunities have been abundant in an age of falling interest rates and rising valuation multiples against a backdrop of steady inflation (which keeps nominal revenues and values rising). These past 40 years have been a dream scenario for owners of capital.

What happens now that interest rates are no longer going down? What if tariffs can help close the trade deficit and reduce the inflow of foreign capital that floods our capital markets? Even if the current system stays in place, the wealth pump will start to diminish. Yes, tech entrepreneurs and venture capitalists will still get rich coming up with new businesses, but the easy money that has been made by private equity barons, corporate executives, real estate investors, university endowments, etc. as they rode a wave of leverage and rising valuations for 40 years should be harder to come by going forward. I agree a new dispensation to target broad prosperity needs to be developed (because the Reagan dispensation no longer works), but I am not sure we should keep reaching back to the 1930s to find the answer. It is likely to be a different dispensation for a different time.