Nixon, Gore, the paths not taken

The end of the postwar economy

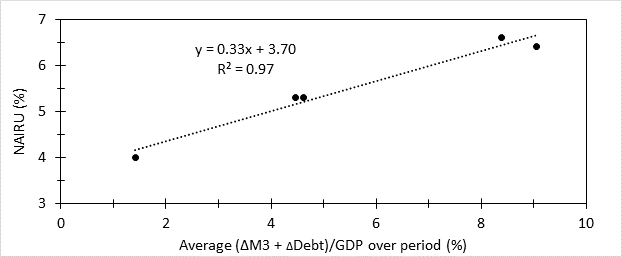

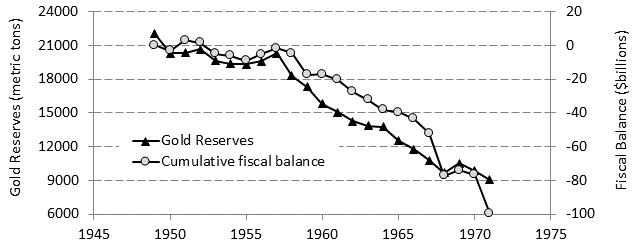

The postwar American economy (1947-73) featured strong economic growth with rising incomes in all income quintiles. I have argued that the end of the postwar economy was caused by stagflation resulting from the end of the gold standard in 1971. The gold standard was ended because gold reserves were falling and would be exhausted before the end of the decade. I argue the decline was caused by fiscal deficits. Despite ongoing budget deficits, President Kennedy proposed tax cuts in 1962, which were implemented by Lyndon Johnson in 1964. At this time, when stock buybacks were forbidden, the fiscal deficit was the dominant factor influencing the money balance, NAIRU, and hence, the inflation driver. Inflation driver is the difference between NAIRU and unemployment and is depicted in Figure 1 as the thick black line. NAIRU values are obtained from the money balance model. According to the Phillips curve concept, when unemployment is below NAIRU (the inflation-neutral unemployment level) the inflation driver is positive indicating an inflationary condition. If this condition is not addressed by contractionary Fed policy, inflation will eventually happen.

{kind=link}

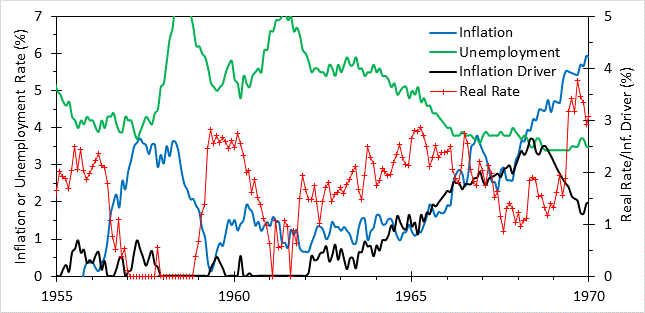

Figure 1. Inflation driver (NAIRU-unemployment), real interest and inflation 1960-70

Figure 1 shows inflation driver began to rise above its 1950’s levels in 1964 and inflation began to rise in the next year. Gold reserves continued to fall until 1971, when President Nixon ended gold convertibility and implemented price controls to prevent the inflation that would surely follow this action. After controls were lifted at the beginning of 1973, inflation began to rise, reaching 7% by September. The Fed began to aggressively hike rates at the beginning of 1973. Fed Funds Rate rose from 5.3% at the start of the year to 10.4% in July, corresponding to a real rate of 4.5% (see Figure 2).

{kind=link}

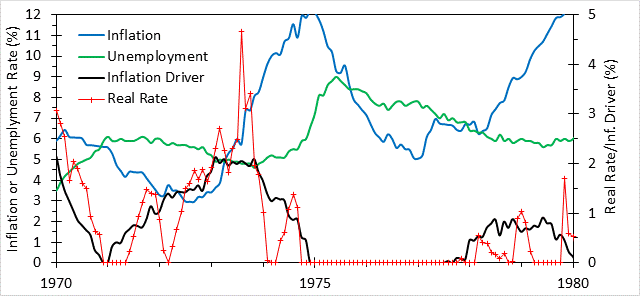

Figure 2. Inflation driver, unemployment rate, real interest rate and inflation 1970-80

Interest rate went modestly higher to 10.8% in September. The OPEC oil embargo began in October 1973 and the economy fell into recession. The Fed started rate cuts in response, reaching 9% in February 1974, by which time inflation had risen so much that real rate was negative (see Figure 2). The Fed reversed course, hiking rates by 400 basis points over the next five months, which pushed real rates positive again. By this time unemployment had started to rise rapidly, and the Fed began easing. Inflation peaked four months later in November of 1974 as unemployment rate shot above 6% heading for a peak of 9% the following May. It was rising unemployment that sent the inflation driver to zero and finally ended the inflation.

The combination of recession and rising inflation was dubbed stagflation. The proximate cause was likely the supply shock from the embargo. OPEC quadrupled oil prices following the embargo, resulting in an increase in the real price of crude oil from an average of $0.55/gal (in 2024 dollars) over 1948-71 to $1.21 over 1974-79. This was followed by a second oil shock due to the Iranian revolution that brought average real crude oil price to $1.93 over 1980-85. This 3.5-fold increase in the real cost of a critical input into the US economy had a devastating impact on US economic productivity. Productivity grew at a 2.8% rate over 1948-73, but only 1.2% over 1973-86. Oil prices collapsed in 1986, averaging $0.96/gal in 2024 dollars over 1986-99. During this time productivity growth recovered to 2.0%.

I cite all this information to support the case that it was the sudden and sustained increase in real oil price that ended the postwar economic miracle. It is instructive to look at the evolution of the price of oil expressed in terms of gold. From 1948-1971 crude oil prices averaged at 2.55 grams/bbl. After the OPEC price hike, price averaged 2.52 grams/bbl over 1974-79 and 2.45 grams/bbl over 1980-85. When expressed in terms of gold, there was no increase in oil prices at all. From this perspective, the ultimate cause of the oil price was the failure of the American authorities to maintain the gold standard, that is, to run balanced budgets during the 1960’s and 1970’s.

The issue of gold outflow was acknowledged during the 1960 election

The question arises, did the economic authorities knew about the risk of running deficits in the early 1960’s? In the third Presidential debate in 1960 there was brief discussion of gold outflows in which Nixon explicitly relates deficits to gold outflows showing his awareness that the country was currently deliberately allowing the gold reserve to fall. During the second 1960 debate Nixon had noted that higher taxes may be needed to prevent budget deficits in the 1960’s. In a foreshadowing of “supply-side economics” Nixon criticizes a Democratic argument that one can fund increased spending through economic growth as something done “with mirrors.” I find this critique eerily similar to George H.W. Bush’s critique of Ronald Reagan’s plan for a second Kennedy tax cut as “voodoo economics.”

Nixon was right in 1960 when he forecasted higher prices as a result of budget deficits. The effect was delayed by the buffer provided by large US gold reserves, however. It was only when the buffer and the 1971-73 price controls ended that prices were free to adjust to the new post-gold standard world. And it was only in such a world that the massive OPEC price hike could be sustained.

The 2000 election, background information

A situation similar to that in the 1960 election occurred again in 2000. Before proceeding I need to explain the Social Security Trust Fund, which was a campaign issue in 2000. Social Security (and Medicare) are funded by payroll taxes. The 1983 payroll tax increase raised the levy on a typical workers paycheck from 6.7% to 7.65% over the next seven years. This generated a surplus of receipts over outlays that helped fill the budget hole opened by the 20-point reduction in top income tax rate and other changes authorized by the 1981 tax cut. This surplus was used to buy special government bonds which were placed into a Trust Fund. Since these bonds were owned by the Social Security Administration which is a government-owned operation, the interest the government paid on those bonds was paid to itself, and the accumulation of this intragovernmental debt was not reported as part of the official deficit. When program outlays began to rise above receipts, which was projected to happen around 2015, the bonds in the Trust Fund would be redeemed by selling them to the public, in which case the program deficit would add to the reported deficit. In fact, there has been discussion in Congress about cutting entitlements, to avoid this deficit, which amounts to scrapping the Trust Fund altogether, without compensation to those who contributed to it over their working lifetimes.

After 1969, the government ran fiscal deficits for 27 years, during which the national debt rose from 28 to 46 percent of GDP. The Clinton administration ran balanced budgets or surpluses during their entire second term, dropping the debt to 32% of GDP. At this rate the national debt could be paid down in a decade. In 2000, Democratic nominee Al Gore ran on a plan he called the lockbox which involved using half of the surplus to pay down the debt, so that when the time came to convert the Trust Fund into publicly held debt the debt increase would be easily affordable and have no adverse effect on the economy. It was a promise to keep faith with the ordinary working people who had paid 7.65% of their pay for their entire careers to build the Trust Fund, by ensuring the government could honor that promise.

The 2000 election, the road not taken

In the first Presidential debate in 2000, Gore explained his plan “under my proposal, for every dollar that I propose in spending for things like education and health care, I will put another dollar into middle class tax cuts. And for every dollar that I spend in those two categories, I’ll put $2 toward paying down the national debt. I think it’s very important to keep the debt going down and completely eliminate it.” Republican George Bush countered “My opponent thinks…the surplus is the government’s money. That’s not what I think. I think it’s the hard-working people of America’s money and I want to share some of that money with you.”

Democrat Gore was the voice of fiscal responsibility in 2000, while Republican Nixon had performed that role forty years earlier. Both men lost the election by razor-thin margins and their opponents, once in power, pursued tax cuts and wars leading to economic disaster. The Democratic victory in 1960 gave us the 1970’s stagflation, while the 2000 Republican victory gave us the 2010’s Great Recession. The fact that these two candidates were from different parties shows that correct policy is not the purview of any one party. Properly steering the ship of state is a joint responsibility of both parties.

Political analysis

To understand this dynamic better I turn to the Skowronek political time model. Both Nixon and Gore were vice presidents to first preemptive presidents and sought to become second preemptive presidents (Nixon went on to do this in 1968). Coming from the party not holding the dispensation, preemptive presidents must operate within boundaries set by the opposition. The first preemptive, who is his party’s first president following the discredited disjunctive president, must hew closely to the new paradigm, trying to stand out by the quality of their administration of the opposing parties dispensation. The Eisenhower administration in many ways represents the heyday of the New Deal Order established by reconstructive president Franklin Roosevelt. Similarly, it was the Clinton administration who made Reaganomics work for the broadest section of the public. Nixon and Gore, who promised to continue the responsible execution of the opposing party’s dispensation, were rejected in favor of second articulative presidents. Coming from the dominant party (i.e. the one who established the current dispensation), second articulative presidents are more willing to push the envelope. Both Kennedy-Johnson and Bush passed tax cuts and began wars in the same year: Vietnam in 1964, Afghanistan in 2001 and Iraq in 2003.

Although both Kennedy-Johnson and Bush showed the same disregard for deficits, the outcome of their rule was very different. For the 1960’s presidents the effect of deficits was inflation, as forecasted by candidate Nixon in 1960. Even worse fiscal irresponsibility by the Bush administration did not produce inflation. The reason for this was the rise of large flows of money out of the economy and into the stock market reflecting increased use of stock buybacks.

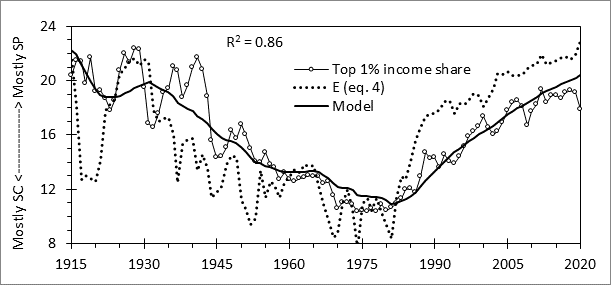

These money flows were made possible by the 1982 legalization of buybacks by the Reagan administration. They reflect the “capitalism=maximizing shareholder value” belief system that is foundational for shareholder primacy (SP) culture. The deflationary characteristics of stock buybacks allow low taxes and inflation (optimal for investors) to exist alongside low unemployment (which minimizes political challenges to the pro-investor order). This serves to concentrate income and wealth at the top (which is the proxy I use to measure the prevalence of SP culture).

{kind=link}

The choice in 1960 was continuation of the New Deal Order (Nixon) or disruption leading to a new order (Kennedy). The people chose Kennedy and that ultimately led to Reaganomics and the rise of SP culture. The choice in 2000 was continuation of a responsible Reaganomics (Gore, McCain) or disruption leading to an uncertain future (Bush).

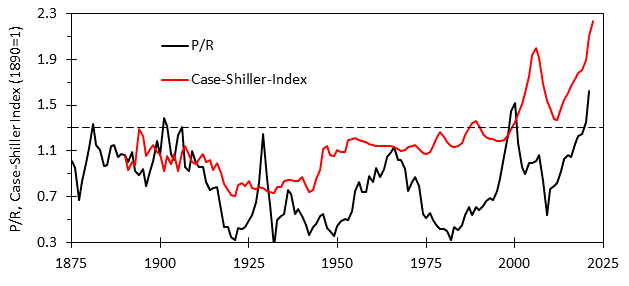

This disruption involves financial instability and the possibility of depression and/or the end of liberal democracy. Tax cuts passed by Republican Congresses over 1997 to 2003 had reduced capital gains tax rates from 28% to 15%. Reducing taxes on profits from asset price appreciation encourages rising asset prices, creating financial bubbles whose unwinding can induce financial crisis. The first “bubble act” in 1997 gave us the tech stock boom and crash, which was followed by a second bubble act in 2003, a real estate boom, and subsequent crash. This bubble deflation led to financial crisis and the Great Recession. A third bubble-promoting action, this time by the Fed in March 2020, has produced P/R valuation extremes in the stock market and on real estate even greater than the previous ones. Before the New Deal eliminated them, the American economy featured semi-regular financial crises spaced an average of 18 years apart. With the restoration of pre-New Deal top income tax rates in 1986 and the subsequent bubble acts, the stage was set for the 2008 return of that hardy perennial, financial crisis. If they are truly back, the next one would be “due” sometime around 2026.

{kind=link}

The outcomes of the 1960 and 2000 elections show that effective policy formation must take politics into consideration as a basic constitutive element. Democrats in 1960 certainly knew that their political success was due to the support of working-class Americans. They must also have known the foundation for their support was their positive experience with New Deal economics, which I proxy by real unskilled wage growth. Inflation adversely affects real wages and so would hurt the Democratic brand. Some Democratic Keynesians, like MMTers today, seemed to think the government could run deficits all the time without consequence. Whether they believed this or not, they acted as if they did and destroyed their dispensation.

The same thing was true of the Republicans in the 2000’s. During the Clinton administration, tax increases and spending reductions, mostly for defense, eliminated deficits, allowed unemployment to reach low levels without inflation, which had not been possible in the 1980’s. As a result, real median personal income growth over 1992-2000 was 2.3%, compared 1.0% over the previous 12 years. Rather than learning from this experience, the Bush administration completely ignored what had been achieved economically in the previous 8 years. They also ignored warnings about the threat of al Qaeda terrorism. Instead, they chose to restore the budget deficit and downgraded the anti-terrorism activity. These choices gave us two failed wars, a wrecked economy and out-of-control deficit spending. The rise of MAGA and Bidenomics suggest that the Reagan dispensation is on its last legs. We may see the establishment of a new Democratic dispensation if Biden wins and Democrats regain control of Congress. If Trump wins, we could see a restructuring of the Reagan dispensation into Republican Fascism, analogous to how Theodore Roosevelt transformed the Lincoln dispensation into Republican Progressivism.