Ziggurats of Finance

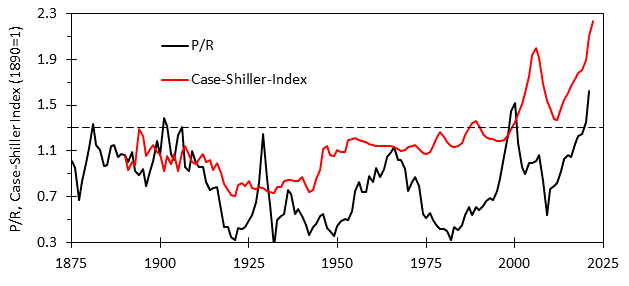

I believe the core problem with America is what I call shareholder primacy (SP) economic culture. Through the operation of SP, American asset markets have developed unprecedented valuations over the past three decades. For example, the “Buffet ratio” (Stock market capitalization as a percent of GDP) has doubled from a peak value of about 1 in the past to around 2, implying the presence of about $30 trillion of additional resources tied up in equity markets that was not so tied up in the days before SP culture. I refer to the accumulation of these resources as the building of “ziggurats of finance.” Such financial architecture is increasingly the legacy of American civilization today, much as the Great Pyramid is for the Egyptian civilization during the reign of Pharoh Khufu.

{kind=link}

{kind=link}

Dividing the estimated $30 trillion in excess stock market value by the current market P/E of 28 yields $1.07 trillion dollars of earnings (3.6% of GDP) that function as “support payments” required to prop up the ziggurat. The evolution of SP culture from 1980 to the present saw the fraction of GDP going to the bottom 90% of Americans as income falling from 55.8% to 44.5%, indicating 11.3% of GDP transferred away from the pre-tax collective earnings of the bottom 90%. Offsetting this decrease were increased government and employer benefit payments amounting to 8.1% of GDP. Thus, the bottom 90% are receiving a 3.2 percentage point smaller share of GDP, providing almost 90% of the support payments for financial monument maintenance. Now, as in ancient times, the resources of ordinary people are extracted to pursue projects of elite vainglory.

Since American is still (I hope) a democracy, American workers, unlike their ancient Egyptian counterparts. should have a say in the size and kind of the monumental architecture that is sustained through their labor. In many of my articles I have documented the cost to ordinary Americans of pursing monument building under SP culture. It has led to stagnant income growth for unskilled workers, leading to reduced marriage rates, increased risk of financial crisis, and contributed to reduced American military power and an inability to build things.

{kind=link}

Were America to move from an SP cultural modality to stakeholder capitalism (SC) modality, that 3.2 percentage points of GDP used for financial maintenance would gradually shift back to the bottom 90%. Note, this is not income redistribution. It happens naturally through the normal market mechanisms. State economic policy is changed so that the construction of financial architecture is impeded. This is done through three mechanisms. First stock buybacks are banned. This removes the ability of companies to directly build higher stock market capitalization by purchasing shares. Second, dividends return to being taxed like wage and salary income as they were before 2003. This discourages companies from paying out all of the profits as dividends since these will be taxed at the higher rates used for earned income. Doing these things channels earnings away from monument building and into economic development. Third, top income tax rates are raised to very high levels. This discourages corporate boards from paying very high compensation to executives since most of it will be taxed away.

The combination of no stock buybacks and high tax rates will severely reduce the use of stock option compensation. Compensation will shift from options to a salary with nice fringe benefits. The net effect of this is to move executive focus away from short-term share price to other metrics. CEOs will act more like sports team managers, finding ways to beat the competition at the game of business, rather than shareholder value maximizers. The result should be more investment in business growth yielding stronger economic growth, but with lower profitability, as happened when we operated under this paradigm in the past.

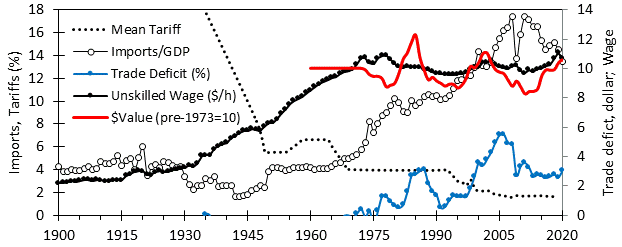

Modern businesses are not averse to investment, but legal stock buybacks mean companies can readily access financial returns requiring that business return must compete with financial returns. Financial returns today are higher than average business returns, which means new investments must meet a higher threshold of profitability than in the past This is one reason why we have seen the rise of platform companies who act as middlemen facilitating business transactions, and new business structures for companies that still sell products in which low margin portions of a business are outsourced (GaveKal 2005, p 6), which has led to the offshoring of manufacturing. These developments haves led to increased ziggurat growth while “hollowing out” manufacturing, making the economy vulnerable to supply disruptions. Firms have sought to retain the most profitable aspects of their business and outsource the less profitable ones. During long bull runs, stock buybacks will produce a higher return from the price rise than the average return on capital. By decoupling executive compensation from share price, you make profitability less, and growth more, important.

A side effect of this policy is a reduction in the importance of finance. For reasons previously discussed, policy engendering SC culture must be implemented during a major economic downturn and stock bear market. Associated with the market decline would be a decline in the number of hedge funds, private equity, venture capitalists, and other financial firms. Restrictions on asset price growth afterward will retard recovery of investment firms. Investor money will be tighter and there will be fewer resources available for “disruptive” investments. Market disruption refers to the restructuring of an existing kind of business in such a way as to extract more profit. After applying a suitable capitalization factor the result in an enormous increase in wealth for the investors (and another brick in the ziggurat). An excellent example of disruption is Amazon. Last year Amazon and Walmart both engaged in the same amount of retail sales. Amazon extracted an additional $30 billion in profit from their retail sales business, resulting in an extra trillion dollars of market capitalization for Amazon relative to Walmart. Thus, a single market disruption built 3% of America’s stock market monument.

What made this market disruption possible was the easy availability of investor funds and government handouts. After all, how did Amazon become successful? It was able to sell books for less than other firms because it did not have to charge sales taxes and was able to operate at a loss for years. This is the same way China was able to replace much of American manufacturing at a time when they were not as competent manufacturers as the firms they replaced. The US firms needed to make a profit, the Chinese ones could operate at a loss. The US firms had to pay for their inputs, the Chinese firms were subsidized. For example, in my own industry of steroid manufacture, I was told around 20 years ago that the Chinese were selling a steroid for less than the cost of the diosgenin1 starting material, and less than our product, forcing us out of that market. Obviously, it was impossible for them to produce a product made from a starting material for less than the cost of that material, the Chinese government was subsidizing them in a similar way to how the US government and VC firms were subsidizing Amazon.

In tech there is the concept of enshittification to describe how a new online platform with an investor subsidy provides a superior service for less than the competitor’s, who, unable to compete and still earn a profit, leave or are driven from the business. Once ensured of their monopoly, they reduce the quality of their offerings (enshittification) as they shift to profit extraction to create the market capitalization that rewards the investors. This is analogous to what China has done. The operate at a loss providing product at a lower cost for long enough to drive the competitors out of business, during which they experience massive growth that allows them to learn by doing, reducing their costs to the point where they do not have to raise price much to achieve profitability.

Now one might rightly note that this is just capitalism. And it is. But it is a capitalism whose objective is not necessarily aligned with economic growth that benefits the public. It can be, but it does not have to be. For example, venture capitalists will naturally favor disruptive businesses since the demand is already there, all the new firm need do it find a way to extract more profit from it, which translates into a big payday when the company goes public. Disruption does not lead to the new categories of demand that generate most economic growth, it merely directs more of the business output towards ziggurat building. In contrast, what China does is use American demand to generate Chinese economic growth and higher wages for the Chinese workers (which helps tamp down unrest). Given the current political climate, it seems high time that America considers how we too can promote economic growth and rising wages rather than market disruption.

I submit that returning to SC culture would be a major step towards this goal.

Diosgenin was used in early steroid manufacture in the West in the 1950’s (we and other firms had shifted to cheaper starting materials in the sixties). The fact that the Chinese were using diosgenin meant there were using an antique process probably obtained from old Western patents (modern processes are unpatented trade secrets) and they still were able to beat our price. The fact that their price was lower than the market price of diosgenin was clear evidence that the Chinese government had their thumb on the scale in a big way.

Being a CEO sucks. When I worked in IT I had full access to executive emails. They are overworked, on medication, sacrificing familial relationships, and a media target. They are also smart and skilled sk can easily take an easier job.

How do you propose to keep the best ceos in their jobs after these tax hikes? Why wouldn't they just quit. Even in my case, after I hit a marginal tax rate of about 20% my motivation evaporates and I'd rather work on hobbies than do what's socially valuable. Art is a lot more fun.

Problems of financialisation I can buy. It is the language of shareholder primacy/stakeholder capitalism I dislike. The “stakeholder” language is used by WEF and ESG types to set up cartel arrangements and evade accountability. It is primed for misuse by activist networks.

The problem is not fiduciary duty to shareholders, it is the incentives facing managers. Financialisation should be critiqued directly. Also, our fiscally strapped states are not going want to on the wrong side of the Laffer curve.