An overview of my thesis in response to an incisive comment

A Substack Notes commenter takes me to task for bizarro views.

Leftists were not happy with President Obama’s performance in office. Ben Cohen writes “The hard Left insisted…that Obama should have done more. I would often ask friends who opposed him how more could have been done.” The response he received was unserious. In a comment I answered this question as follows:

What he (Obama) could have done, was, when he suspended his campaign and went to Washington because of the financial crisis, he could have urged Democrats to Congress to not support the TARP, which was a Republican-created solution intended to help the investor class. A majority of Republicans opposed that bill proposed by their own president. Democrats should have joined them.

Second, after he won the election, but before inauguration, he needed to meet with Bernanke and make it clear he was opposed to the sort of actions (i.e. QE) Bernanke had suggested in his 2002 “helicopter speech” the Fed could do to stave off deflation (which would be very bad for financial markets).

Two things Obama could have done, that would be truly transformational in the way FDR was. But he and his party were too deep into neoliberalism and accepting of other Republican propaganda.

In response, Nathaniel Merchant wrote:

Your “two things” are your pet theories and not at all a sign of “neoliberalism”. But of course, it’s the silly season of American politics so we get bizarro takes like this.

This is a perfectly reasonable comment because it is not clear what I am talking about here. I made the post to raise curiosity about what I am talking about among people who would agree with the sentiment that Obama did not do enough. Perhaps a reader might check out my substack to see what this yahoo was talking about. After thinking about this response, I decided I really need write a post in which I explain my take on neoliberalism, and why I suggested a rather “bizarro” action could have been taken.

I have a cultural take on political economy. The culture underlying the American political economy at any time falls into two archetypes. The first variant, “shareholder primacy” (SP) was asserted by economic and legal scholar Adolf Berle in 1931, “all powers granted to a corporation or to the management of a corporation … [are] at all times exercisable only for the ratable benefit of all the shareholders as their interest appears.” The second variant was asserted in response to Berle by Harvard Law Professor E. Merrick Dodd, who noted that “there is in fact a growing feeling not only that business has responsibilities to the community, but that our corporate managers who control business should voluntarily and without waiting for legal compulsion manage it in such a way as to fulfill those responsibilities.” He argued for “a view of the business corporation as an economic institution which has a social service as well as a profit-making function.” That is, a corporation has a responsibility to stakeholders other than shareholders, a view that may be called “stakeholder capitalism” (SC). This debate was an open issue at the end of the twenties boom. Two decades after his 1931 article, Berle acknowledged that it had been resolved in favor of stakeholder capitalism:

Twenty years ago, the writer had a controversy with the late Professor E. Merrick Dodd, of Harvard Law School, the writer holding that corporate powers were powers in trust for shareholders while Professor Dodd argued that these powers were held in trust for the entire community. The argument has been settled (at least for the time being) squarely in favor of Professor Dodd’s contention.

SC was still prevalent in 1981, as indicated by this statement from the Business Roundtable:

Corporations have a responsibility, first of all, to make available to the public quality goods and services at fair prices, thereby earning a profit that attracts investment to continue and enhance the enterprise, provide jobs, and build the economy. The long-term viability of the corporation depends upon its responsibility to the society of which it is a part. And the well-being of society depends upon profitable and responsible business enterprises.

Sixteen years later, the Business Roundtable asserted that the principal objective of a business enterprise is to generate economic returns to its owners. Business philosophy had come full circle, back to Berle’s 1931 position. These changing views of the purpose of a corporation illustrate how business culture changed from primarily SP around 1930 to SC during the 1950’s through the 1970’s, and then back to SP after 1981.

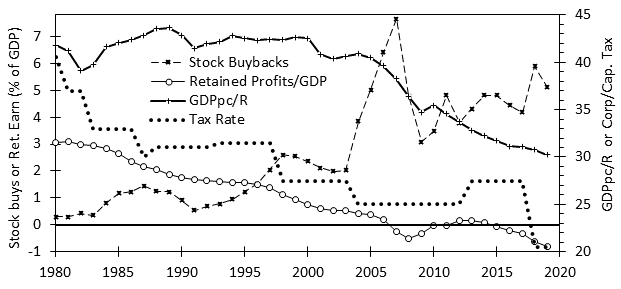

Shareholder primacy holds that economic activity is undertaken for the purpose of enriching shareholders. Thus, the rising trend in stock buybacks since 1980 shown in Figure 1 is indicative of action by corporate managers in support of this objective and is a clear manifestation of shareholder primacy. Another example of action taken for the benefit of shareholders was tax policy, specifically the declining trend in capital gains and corporate tax rates. See this figure for a plot of the average of these tax rates. This figure also shows something called enterprise premium which is the additional return available from running a company as opposed to investing in financial products like stocks. After 1980, enterprise premium went to zero or negative on average, showing a strong bias in favor of financial asset holders (like shareholders) over entrepreneurs, managers and employees engaged in business. The result of corporate and government bias towards shareholders (as called for under SP culture) has been outsized returns on the stock market, which has created a new paradigm for stock market behavior. Twenty years ago I developed a model for stock market cycles based on 200 years of history. In 2014 the stock market violated the two-century pattern by moving strongly above where stocks had traded historically. The cause of this deviation was the appearance of unprecedented levels of stock market manipulation though stock buybacks and QE, which drove the market to incredible heights. So the idea of shareholder primacy first came to my attention through unprecedented stock market behavior.

{kind=link}

{kind=link}

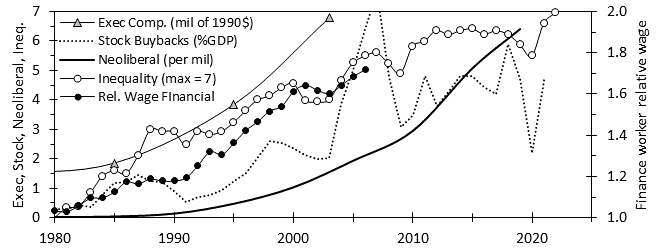

Since shareholders are investors, putting them center will necessarily prioritize financial markets over the goods and services economy. The result has been what is called the financialization of the economy. This trend is illustrated in Figure 1 by a plot of the wages of financial workers relative to other workers with similar educational qualifications. But how did it come to pass that corporate executives and economic policymakers came to prioritize shareholder interests above all else, when there was a time when they did not? The process whereby this happened is described here, but simply put, corporate executive interests were deliberately aligned through the adoption of stock option compensation, which directly incented executives to maximize share prices. This was only possible once the top tax rate was reduced from the 70-90% levels of the 1940’s through 1970’s to much lower levels after 1980. The result was a rapid rise in executive pay as shown in Figure 1.

Figure 1. Indicators of shareholder primacy culture: trends in stock buybacks, executive compensation, financial worker compensation relative other workers with similar education, and income inequality. Also shown in the trend in use of the word “neoliberal” in written work as shown by Google N-gram.

In a world where executives are earning two to five times what they used to, the managerial feedstock for executives come will also come to earn more, simply to maintain amity in an executive’s management team. Also, if financial and managerial professionals are making more, those professions, such as medicine, which traditionally have drawn very high-quality entrants, will necessarily need to show income rises relative to the rest of population. The result of these mechanisms will be to increase wage disparities among educated workers. This is manifested in Figure 1 by an income inequality measure, which has risen steadily since 1980.

At the same time, a flat or negative enterprise premium dis-incents investment in capital intensive enterprise, leading to a phenomenon known as deindustrialization. A decline in capital-intensive business means fewer good jobs for unskilled working-class people. The reason for this is that in a capital-intensive business like chemical or pharmaceutical manufacturing, where I spent my career, labor is a relatively small contribution to cost of goods, the cost of inputs and capital dominates. Thus, it is more important that the process run smoothly than each element of the production process runs at minimum cost. When a single mistake by an ill-trained operator can ruin a million-dollar lot of your product, it is imperative that the workers employed be adequately trained and motivated to perform well. It makes sense to employ untrained workers for low-skill jobs at your company and train the best of them for higher-responsibility jobs in-house. Henry Ford discovered this when he needed to get reliable workers to operate his high-productivity assembly-line technology, He found that doubling high-quality workers pay allowed him to retain the kind of workers he needed to keep his operation running as intended.

{kind=link}

The existence of industry “vacuuming up” high quality workers meant other kinds of employers had to up their game and offer better wages to keep their best employees. The result was a trend of rising wages and a favorable labor bargaining position. Under such conditions, unionization makes sense, and this provides an additional mechanism ensuring that the fruits of economic growth are shared between investors, management, workers, and customers (i.e. stakeholders). Such a stakeholder culture world with a flatter income distribution is characterized by a low level of inequality in Figure 1.

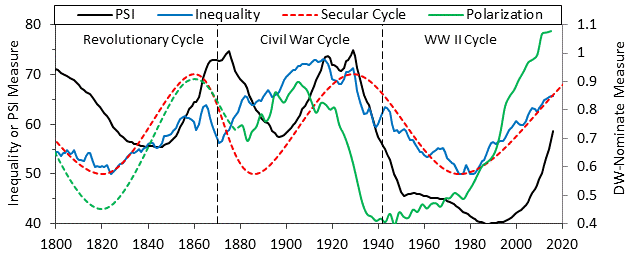

That is, economic policy that produces a positive enterprise premium (and full employment) leads to an environment in which something like stakeholder capitalism can be maintained. In my development of these ideas, I focused on executives as an evolving population and used cultural evolutionary tools to describe how economic culture evolved from SP to SC and back to SP over the past century. I employ income inequality as a proxy for the relative level of SP culture. See this figure for a long-term perspective on inequality, showing how it was high around 1930 (when culture was SP), low in the 1940’s-1970’s (when culture was SC) and is high again today (when culture is SP).

{kind=link}

If we bundle the financial wage, CEO compensation and stock buybacks together we would see a rising trend consistent with the rising trend in inequality. All of these phenomena are related to the shift from SC to SP culture. Since “culture” is difficult to quantify, I have to use some measurable thing as a proxy for it. In principle, I could use any of these things for my proxy. I use inequality because it is also a proxy for the secular cycle, which is the historical framework I use in my work (see chapter 1 in America in Crisis for a fuller explanation).

Figure 1 shows as the bold black line a parameter called neoliberal. This refers to the incidence of the word neoliberal (or variants) in written works over time, as measured by Google N-gram. This is yet another possible proxy for SP culture, except it lags the others. The lag makes sense because it took time for intellectuals to realize that the political and economic world had started to change in the 1980’s, to develop terminology to describe this change, and then for it to spread. Nevertheless, the trend in use of the word neoliberal provides another measure of how SP culture was permeating the minds of writers.

Economics writer Noah Smith complains about how economic policy is discussed:

I’m not happy about the fact that America thinks of economic policy in terms of number of jobs created. It’s not a very clear or meaningful way to think about policy — overall employment is more a function of macroeconomics than micro, so we should really be talking about the results of policy in terms of wages and incomes. But “jobs jobs jobs” is how the game is played, and so we should just expect any politician to talk about that a lot, without assuming that “job creation” is the true underlying economic rationale for any policy.

What should matter in a discussion about economic policy is the impact of the policy on wages and income as I highlighted in italics. But what is actually talked about is job creation. This framing of economic discussion as about job creation is another manifestation of SP culture. Job creation simply means making the SP economy bigger. Noah observes that Biden has been doing this, but real wages have not been rising as a result. Economic policy that creates jobs accords with SP culture, while raising wages or incomes would be to move away from SP, and is culturally taboo, so economic policy discussion studiously avoids it. On the left, MMT enthusiasts argue for a much more extensive industrial policy to create lots of jobs via a green energy economy, arguing that it can be financed with deficits. They have been led to believe this was possible because of the very low inflation we saw in the 2010’s despite the continuous presence of substantial deficits. Yet we have just gone through a period of large deficits and inflation ensued.

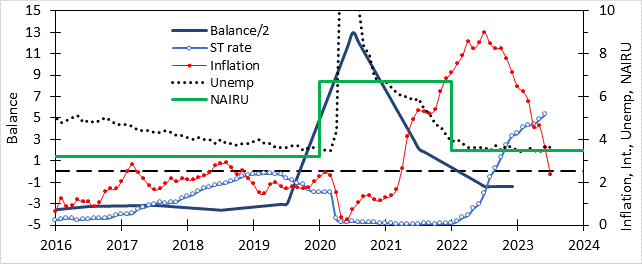

The reason for this, as the balance model makes clear, was that deficits during the last decade were more than offset by large expenditures for stock buybacks and dividends which pulled the money added to the economy by deficits out of the economy, sending it into the stock market. The result was a net flow of money out of the economy, as shown by the negative value for Balance in this figure. This low value for Balance means a low NAIRU, well below the level of unemployment, meaning there were no inflationary forces present. The 2010 deficits did produce inflation, it just happened in the stock market, not the real economy. It is possible to run sufficiently large deficits as to overwhelm the financial flows. This is what happened in 2020 and 2021, as shown in the figure. Balance moved sharply into positive territory, NAIRU went up, and as unemployment fell below this higher NAIRU, inflation appeared. Large-scale deficit spending ended in 2022, Balance fell back down and NAIRU with it, and inflationary forces subsided. If we followed the MMT prescription, inflation would return.

{kind=link}

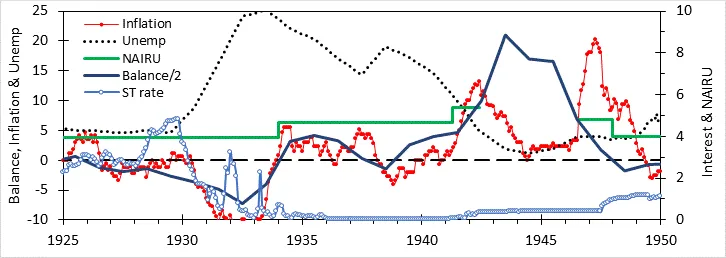

The idea of using government spending on green energy to directly boost economic growth stems from the effect WW II had on the postwar economy. America went into the war with a deeply depressed economy with double-digit unemployment. War expenditures were enormous, resulting in a 55% expansion of real GDP over 1940 to 1946—a 7.2% growth rate. Over the next 27 years, GDP would continue to grow at 3.8%, a historically fast pace. Compare this to the 2.3% annual growth for WW I (1916-19) and 3.5% for the postwar era (1919-29). Those on the left note the New Dealers employed price controls to keep inflation in check during WW II, while inflation had been allowed to run wild during WW I, which likely explains the stark difference in wartime growth rates. What they do not talk about was the extraordinary levels of taxation present during the second war and which persisted for decades afterward. What created the postwar miracle was not the WW II spending, that ended with the war. It was the high top marginal tax rates, which promoted SC culture, and the rapid return to fiscal balance after the war, which sent Balance down, reducing NAIRU, giving low inflation, low interest rates and low unemployment during and after the war. Maintaining this sort of “Goldilocks economy,” when coupled with SC culture, produced the sort of wage and income growth Noah complained wasn’t being discussed. I note that we have had Goldilocks economies under SP culture, in the late 1990’s, late 2010’s and today, but with no sustained increase in real wages, or decline in inequality. You need the SC culture to obtain this sort of outcome.

{kind=link}

{kind=link}

But to get that SC culture, and keep it, requires a high top tax rate, which is taboo under SP culture. High top tax rates that helped create SC culture were initiated under a Republican administration in 1932 and increased to around 90% for WW II. In both cases, these actions were in response to crises. Had Democrats in 2008 not supported the TARP it was entirely possible the financial system could have collapsed, and the Dow fall to the neighborhood of 4000 before the end of the year, which would certainly qualify as a crisis. This collapse would have happened during a Republican administration whose rescue plan was rejected by Republicans. Wealthy patrons of both parties would be demanding action. A suitable time-limited program to deal with it, if accompanied by large tax increases, would score as deficit-reducing over a 10-year period and so could be passed under reconciliation, overriding any Senate filibuster. This is what my post referred to. Of course, it would never have happened, I myself would have opposed it. I was still fairly neoliberal in my thinking at that time and enthusiastically supported Obama’s policy preferences (buying stocks shortly after the TARP was passed). I had believed that Clinton’s fiscal policy, creating a Goldilocks era, was going to create a boom in productivity and restoration of rising wages. When this did not happen, I blamed a lack of leading sectors in my 2004 book, not the wrong economic culture.

So Merchant is justified is calling my post bizarro nonsense, which it is when viewed from a SP framework (which is the dominant viewpoint today, and very likely his own).

I agree with most of this except for your characterization of the MMT position which explicitly connects inflation to fiscal policy: that cost push inflation occurs at the boundary of real resource (including labor) availability with the solution being to tax demand out of the system.

Certainly your observation about “where the money went” during the post Great Financial Crisis period is correct: asset inflation, in part because of the low tax regime especially in the upper segments of the income and wealth distributions where relative propensity to spend is low in goods but high in assets — and this problem only gets worse as inequality rises.

The only thing I would add to this excellent analysis is that culture of any kind, including SP/SC is CREATED by people, but all people are not equal in the creation of culture, and the power to influence/shape culture is not constant over time.

This raises interesting questions (which are beyond the scope of your current research, but interesting nonetheless) such as how and why did power shift in the early 1930's to allow FDR to set in motion so many laws, rules, and regulations that supported the flourishing of SC (suppressing the SP of the 1880's to 1930), and what how and why did power shift in the late 1970's to allow Reagan to begin the process of deleting/changing those laws and rules to begin to favor SP over SC. Moreover, what factors contributed to the Democrats under Clinton and Obama to continue to solidify SP rather than counteract it.