Looking at the stock market in terms of money flows

A question often asked is what happens to the money “tied up” in the stock market during crashes. Substack economics writer Noah Smith provides an answer this question using an example:

Suppose there are 1 million total shares of stock in Noahcorp, but that only 1000 shares of Noahcorp get traded on any particular day. And most Noahcorp shares just sit in people’s accounts and never even get traded at all. Now suppose that the 1000 shares that DO get traded go for $300 a share. Mark-to-market accounting means that we value all 1 million Noahcorp shares at $300 a share, including all the ones that never get traded. So the total value of all 1 million shares of Noahcorp — which is called Noahcorp’s “market capitalization” or “market cap” — is $300 million.

Now suppose that tomorrow, those 1000 Noahcorp shares get traded for only $200 a share. The mark-to-market value of the traded shares and the non-traded shares alike goes down to $200 a share. So Noahcorp’s market cap goes down to $200 million.

Smith describes a $300,000 exchange among Noahcorp shareholders giving rise to a $100 million loss in the value of Noahcorp. The total money exchanged was far less than the change in Noahcorp’s value. Clearly, it does not balance.

This example is an extreme one. Let’s now imagine a more common scenario in which 10,000 shares trade and the price falls by 2½ points. Here roughly $3 million changes hands and the value of Noahcorp changed by $2.5 million. Here there is a rough correspondence between the two values and the notion of a “flow of money out of Noahcorp” makes sense. In general, whenever there is a large change in price, wealth changes represented by changes in market cap will be larger than the amount of money traded and financial wealth will have been created out of nothing or vanished into nothingness.

However, stocks rise and fall over time during which both wealth creation and destruction will take place, which will cancel each other out to some extent. In addition, when considering changes to the market capitalization of collection of stocks such as those in the S&P 500 index, cancelations will occur across stocks as well as over time. This means that while it is invalid to account for short-term price fluctuations in a single stock using money flows, such a concept could have utility when considering average flows over longer periods of time in a stock index.

To get a handle on this I estimated the amount of dollars changing hands and the change in S&P500 index capitalization each day over the period from Jan 3, 2007, to December 15, 2022. Approximately 965 trillion dollars changed hands over this period, resulting in market capitalization rising by $302 trillion over 2169 up days and falling by $282 trillion over 1847 down days. The net effect of all this trading was to increase market capitalization by $20 trillion. Just 2.1% of the money changing hands led to the long-term change in market capitalization.

Next, I looked at the dollars changing hands each day as compared to the change in capitalization. I found that 81% of the time the change in capitalization was less than or equal to the money changing hands. That is, 81% of the time, the trading day resembles the second scenario given above in which dollars changing hands can account for all the change in market value. The other 19% refers to days when this is not true. On these days, wealth was being created or destroyed as in Noah’s example. I next looked at the effect of averaging these values over time. I found the change in market capitalization over a four-week rolling period was always less than the net amount of money changing hands. This suggests that if we focus on trend changes over periods of a month or longer, a money flow type analysis could be used to account for changes in market capitalization. That is, a change of $X in market capitalization from one monthly average to the next represents a flow of money into or out of the market over that month.

To imagine this physically, we define a pool of money called the “churn” which represents a pool of cash and shares circulating among stock investors. Money equal to the proceeds of all stock sales over the averaging period flows into the churn. Countering this is an outflow from the churn equal to the total expenditure for stock purchases made during the same period. Money also flows into and out of the churn from the real economy or other financial markets in such a way that the churn is always above zero. Inflows from the real economy can come from new investor money such as 401(k) contributions, reinvested dividends, and stock buybacks, The latter two comprise the “financial flows” in the Balance quantity that I propose plays a significant role in inflation. Outflow may go into other financial markets, cash, or into the real economy. To make the flows balance out we have to imagine the churn to contain the net effects of at least four weeks’ worth of trading. This is physically unrealistic, stock trades clear in much less time, but it is necessary to average out the semi-random wealth creation and destruction that is an inherent element of financial markets as Noah describes.

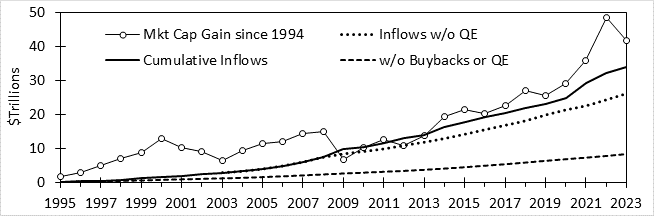

A money flow analysis may be of interest if it yields insights relevant to stock market valuation. After all, a version of money flow analysis is used as a technical analysis tool. To this end Figure 1 presents a plot of the rise in S&P500 market capitalization from a 1994 baseline and cumulative inflows into the churn coming from stock buybacks, dividend payments and Fed QE purchases. For the figure I assume that shareholders re-invest all their dividends in stocks rather than spend it, which of course is not always the case. For QE, I assume that Fed buying leads to reduced return prospects for the purchased asset class, so that the former asset owners use the proceeds to acquire new assets with higher return, displacing a new category of asset holders into higher-return assets and so on until the new money injected into the financial system from the Fed finds its way into the stock market as the highest-return asset class.

Thus, the cumulative inflow line in Figure 1 shows a maximal value for this quantity that holds only for 100% dividend re-investment and 100% of QE ending up in the stock market. Nevertheless, the figure generally provides a lowball estimate for the stock market capitalization and seems to act as sort of floor on stock market values, suggesting it could be used as an estimate for where the market could go in a downturn. Most of the time, the market trades at values well above this value, reflecting new investor money flows, but in bear markets, as investors take their chips off the table, what would be left are the institutional money inflows.

Fig. 1. S&P 500 marked cap rise compared to cumulative dividends, buybacks and QE

Figure 1 suggests that institutional inflows into the stock market represented a smaller share of the gains before the 2008 crisis than afterward. To the extent that cumulative inflow provides a “safety net” for the market, policy such as the cut in business taxes in 2017, which redirected hundreds of billions of dollars away from the government and into the stock market, and the second round of QE begun in March 2020 helped fuel a rise in asset values. This shows how under neoliberalism (defined as the politics associated with shareholder primacy culture) the government actively aids the investor class.

Using the insight provided by cumulative inflow, we can estimate where the market might drop should a recession happen this year. A decline in market capitalization to the cumulative inflow line is consistent with an S&P500 value of about 3000. With the Fed now employing QT operations (which reflect a flow out of financial markets) I presented a cumulative inflow line without QE additions. Should a recession happen, and it becomes clear that there isn’t going to be a return to QE, a larger decline to the dotted line might occur, which corresponds to an S&P500 level around 2400. These two values provide a range for worst-case scenarios in the event of a more serious bear market in 2023.

This is a far cry from what my previous stock market valuation method called for. Under this system I had projected (in 2000) a secular stock cycle bottom around 700-900 in 2010-14, which I refined in 2002 to around 1000-1200 in 2018-2022. This old model was predicated on the idea that profits not paid out as dividends would be reinvested into the business, not used for stock buybacks, and that the government does not create trillions of dollars and inject them into financial markets. If these two flows are removed the resulting “floor” shown in Figure 1 is about 1200, consistent with P/R valuation. That this was not going to happen became evident after 2014 when market action continued to break with the historical pattern, leaving me confused. It has only been in the last year after doing the research for America in Crisis and development of the money flow inflation model, that a new picture on how the modern stock market might work has come into focus.

One can think of stock values in two ways. One is to consider stock price as the value of a share of the underlying business, which it technically is. This becomes directly relevant when a company is purchased with cash such as Elon Musk’s recent purchase of Twitter, which established that Twitter stock was worth $53 per share. The rest of the time it is the theoretical basis for fundamental analysis in which the underlying company is valued as a business and then divided by the number of shares outstanding to estimate share value.

The other way is to think of shares as an investment product whose price is the result of supply and demand in the stock market. Here a stock is worth what investors think it is worth, as indicated by the price at which they actually buy the stock. This idea forms the basis for technical analysis. Technical analysis examines price movements over various time periods to assess whether investors collectively believe a stock (or the market) is undervalued and so will rise in the future, or overvalued and so will fall. Crypto assets like Bitcoin are an example of an investment product whose value is purely based on technical analysis.

My old stock market valuation tool, P/R, was a fundamental valuation tool, as are things like CAPE or Tobin’s q. R was sort of a book value which took inflation into account. It failed once stock buybacks started becoming a thing and even more so with QE. Profits spent on buybacks are being used to directly boost stock price by increasing demand for shares, rather than indirectly by increasing the amount of productive capital possessed by the business, which is what fundamental valuation seeks to measure. Hence, P/R does not capture the rise in the market value resulting from stock buybacks, whereas the flow analysis in Figure 1 does. As Figure 1 shows, the difference between where the market is trading and where it would be if large-scale stock buybacks and QE were not a thing (and P/R valid) is very large.