Can a new Democratic order address the American Crisis?

The stumbling block to a solution for the problems of inequality, polarized politics, and climate change is the even distribution of the wealthy between the two parties.

There has been a growing feeling that something is wrong with the direction America is heading since the turn of the century. The idea that we live in a time of crisis has gained currency in recent times. America in Crisis is an analysis of the political and economic dynamics responsible for this feeling. I use a cyclical concept, not William Strauss and Neil Howe’s generational cycle referred to in the previous link, but Peter Turchin’s secular cycle, with corrections that address some of the issues raised in the cited review. I believe a major driver of society is cultural evolution and talk about it a lot. There is also quite of bit of political, economic and financial discussion as I believe these disciplines are also very important to understanding what is going on. I wrote up my analysis in a book with the same name as this substack. I cover some of the material in the book here, plus new insights as they occur to me. For easier comprehension it may help to read posts in sequential order so that when an older post is referenced there is some familiarity.

Back in April I wrote a post suggesting a way a political resolution of the current crisis might happen. I suggested that Biden may turn out to be a Reconstructive President, beginning a Democratic dispensation that replaces the Reagan Republican dispensation. I noted that neoconservatives, one of the three core Republican constituencies Reagan had identified, no longer have a place in the new MAGA Republican party. I also noted that MAGA Republicans were not as obeisant to corporate interests as the Reagan conservatives had been. With the recent victory in Ohio and the Georgia indictment the Republicans are increasingly looking like losers in 2024, which could further weaken corporate allegiance to the GOP. I also noted demographic trends which favor Democratic prospects going forward.

The defining feature of dispensations is they start with one party winning the presidency for three or more sequential terms. The Jackson dispensation began with three Democratic victories. Lincoln got six, FDR five, and Reagan three. There are some earlier indicators of a developing dispensation before the confirming third electoral victory. One is the last president under the old dispensation, called a Disjunctive president, serves only a single term, usually by losing his reelection bid, and has a reputation as a failure afterward. Donald Trump seems to fit this bill.

Another indicator is that Reconstructive presidents typically win their second terms by a popular vote landslide. This is not definitive, because landslide victories can also happen for Preemptive presidents, the alternative to Reconstructive. Table 1 shows the ten two-term presidents who had the potential to be Reconstructive and for whom we have popular vote results. Four of them were elected to their second terms in a plurality or narrow majority, one of which (Cleveland) did not even win re-election but came back a won a second term in the next election. All of these were Preemptive presidents. Of the remaining six who won their second term in a landslide, four were Reconstructive. Were Biden to win 54% or more of the popular vote next year, this pattern suggests a greater likelihood that he is a Reconstructive president.

Table 1. Popular vote percentages for Reconstructive versus Preemptive presidents.

Recent economic developments are favorable to the President’s re-election chances. A massive expansion in the workforce has created a non-inflationary expansion in aggregate demand that will likely prevent the long-expected recession from coming. A second month showing low (3.3%) inflation over the prior year is creating a perception that inflation is ceasing to be a problem. Looking at inflation rates over shorter periods of time shows a strong deceleration of inflation: 2.9% over the past 9 months, 2.6% over 6 months, and 1.9% over 3 months. It seems likely we will be seeing headline inflation numbers around 2% this fall. Employment growth has run at 2.2% over the last year, compared to annual growth rates of 1.2% to 1.9% during the four years before the pandemic.

Falling inflation means business is losing pricing power, while employment growth implies continued strong labor demand which should translate into continued nominal wage growth, which as inflation subsides should turn to real wage growth, as it did before the pandemic. The lack of real wage growth has been suggested as a reason for Biden’s low favorability ratings. If so, then the expectation would be for the President’s favorability numbers to rise, while Trumps numbers may fall further as the difficulties his legal troubles create for Republican electoral prospects become clearer. These trends plus the shift in generational makeup of the electorate make a big Democratic victory more likely. This modestly improves the probability that Biden has indeed established a new Democratic dispensation.

This post will assume this to be the case. In my previous post on this topic, when I considered this possibility, I mostly focused on what could happen to the Republican party. I was most interested in the possibility that the appearance of dominant Democratic party would result in political restructuring leading to the creation of a politically viable party willing to sacrifice the interests of the investor class in order to benefit working people. The reason for this focus was because I am a schmaltzy optimist at heart and like happy endings.

But now I will assume that no political restricting happens. The GOP remains intact and becomes a regional party like the Democrats did after the Civil War, only winning the presidency when they nominate a leader from an establishment-friendly Republican faction analogous to the Bourbon Democrats after the Civil War. Post-pandemic political reality is written by a dominant neoliberal Democratic party.

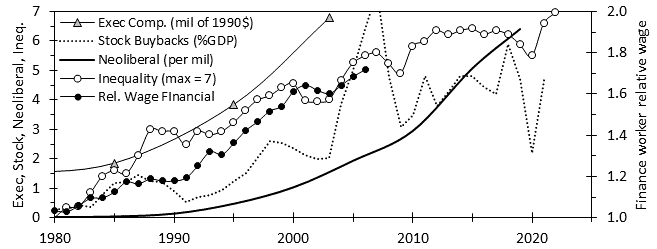

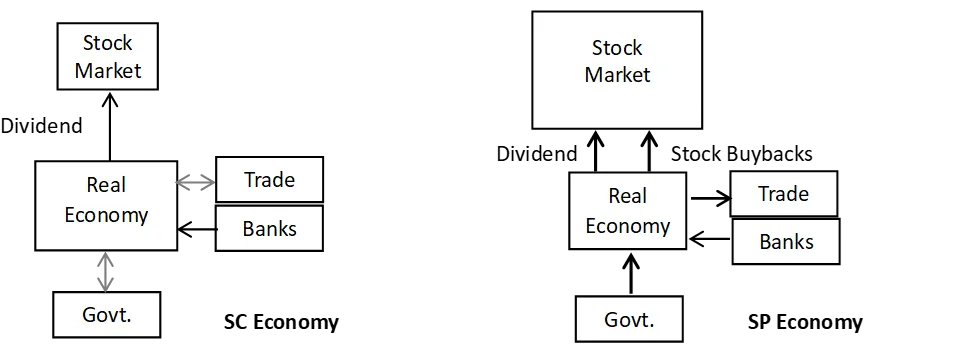

By “neoliberal” I mean a supporter of SP business culture. This definition for neoliberal comes from the lagged correlation between the rise in use of the word neoliberal and manifestations of SP culture like inequality, financialization and stock buybacks. A neoliberal party in charge means no very high marginal tax rates on high income earners that selects against SP culture. It means continued overreliance on inflation control provided by the Federal Reserve. As shown by my inflation model, under a fully developed SP economy, inflation control is mostly handled by large money outflows from the real economy to foreign and the financial economies via trade deficits, dividends and stock buybacks that remove dollars added by deficits from circulation, suppressing inflationary forces. This is manifested as an economy with a low NAIRU, which enables low inflation despite low unemployment and large fiscal deficits. The cost of such a policy falls on working people through suppression of real wage growth. This is possible without electoral consequences because the working class is neatly split between the two parties on racial and cultural grounds, negating their political power as a class.

{kind=link}

{kind=link}

Baring the outbreak of a major war, which could serve as a conduit to something like SC culture as happened in WW II, a Democratic dispensation would remove the threat of fascist dictatorship, but low top tax rates will remain and with them the current levels of high inequality, political polarization and sociopolitical instability, as measured by PSI. High top tax rates (≥70%) cannot be enacted by Democrats because too many of their coalition and all of the Republicans would oppose it. Republicans have long ceased having a near-monopoly on the resources of the very wealthy.

{kind=link}

Right now, the focus of the Democratic economic program is to create as many jobs as possible, driving unemployment to extreme low levels in order to produce labor shortage, which they hope will raise the fortunes of working people in time for next year’s election. They way they seek to do this is economic stimulus in the form of the Infrastructure Investment and Jobs Act and the Inflation Control Act totaling $2.1 trillion in new spending. This additional spending will likely result in a 2023 deficit about 0.5% of GDP higher than in 2022, which may push the money balance into positive territory for 2023 and create a slightly more inflationary economy. This may be why the Fed is continuing to raise interest rates despite the current falling trend in inflation mentioned above.

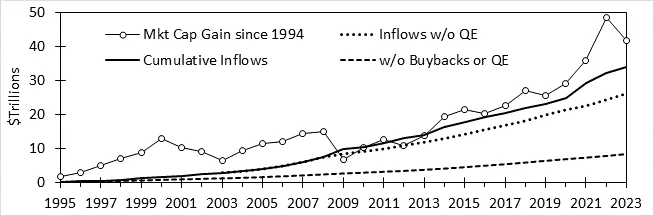

As interest rates rise and inflation falls, the real return available from ultra-safe T-bills becomes more and more attractive. In the 30 months since inflation began to pick up, the real return on stocks has been about 2%, about the same as the current real return on T-bills. Before corporations and the Fed began to practice market manipulation in a big way by injecting money into the market via stock buybacks and QE, long term real return from equity was approximately equal to earnings yield (the reciprocal of P/E). Consider the period from the end of the postwar bull market in December 1968 to the October 2007 peak just before the 2008 crisis, after which all the QE and the largest buybacks happened. The average P/E over this period was 17.4, giving an earnings yield of 5.8%. Total real return on stocks over that period was 5.7% compared to a safe return of 1.2%, giving a 4.5% premium for taking on the risk of equity investments. At present the earnings yield is about 4.1%, while the safe rate will likely reach 3% by this fall, providing only a quarter of the old premium in an expensive market.

{kind=link}

Continued stock price rise will need strong earnings growth, which would forestall wage growth. Falling real wages is a problem for Democratic electoral success because of the strong white working class support for MAGA. As this figure shows, after decades of no change, real wages rose during Trump’s time of office, but then fell under Biden. Not only do his working class supporters like his pugnacious, burn-it-all-down attitude, but they could see benefits in their pocketbooks when he was in office and bad times under Biden. Democrats need real wages to stop falling and start rising. Nominal wages already are rising due to strong demand for labor helped by Democratic stimulus. This needs to continue while at the same time employers need to be denied pricing power so inflation does not rise. Fed interest rates are having this effect, but they work partly through expectations. Business expects the interest rate hikes will eventually bring about a recession. Companies are loathe to hike prices in the face of a recession for fear they would lose market share to a competitor who did not raise prices. But when the recession doesn’t materialize the effectiveness of expectations will diminish, unless something else happens that causes the same effect.

{kind=link}

That something could be a weak stock market. On occasion, a bear market happens with no associated recession, examples include the 1966 bear market, the 1987 crash, and last year’s bear market. Bear markets since WW II have averaged about 30% decline, making last year’s bear, at 27%, pretty typical. With the market nearly recovered to its old high, there is room for another typical bear market. Were such an event to happen, it would bring out the greybeards opining on how this era is reminiscent of the late 1960’s and early 1970’s market cycles. This kind of narrative would likely affect expectations, serving to sustain the fear of recession while government stimulus is raising employment, keeping demand high and holding recession at bay. Such an outcome could give rising real wages for years, aiding Democratic electoral prospects.

If Democrats win next year and regain control of the government, it would be very much in their interest to repeal the 1997 tax cut or 2017 tax cut, or better still, both. Doing this would almost guarantee a bear market, that, with the current level of stimulus, will probably be a repeat of 2022, but without the inflation. Were this to happen, total real stock return that is not competitive with safe returns over a sustained period will become a reality. This is the process through which secular bear market psychology develops. Shifts in this sort of market psychology are responsible for the secular stock market cycles. Sometime this shift happens quickly because of a market collapse, as happened after 1929 and 2000. Other times it is a slow process like the 1966-1973 bull-to-bear transition period, which saw two short-lived periods of speculative frenzy, the late 1960’s go-go years and the subsequent “Nifty Fifty” era. These ended with the massive 1973-74 bear market, few years after which Business Week proclaimed the death of equities. The idea here is to engender an increasingly bearish market psychology despite objectively good economic performance.

The Fed will be unable to slash rates or restart QE to address stock market doldrums because the economy will remain in an inflationary situation, as rising interest rates drive up government interest payments, deficits, and Balance. At some point Democrats will have to deploy the platinum coin option to pay down some of the US debt in order to reduce interest expenses, keeping Balance from rising too much. The way this works is the Fed buys newly issued debt and exchanges it for platinum coins. The interest the government pays on this debt goes to the Fed, who returns it to the government. Thus, the effect of higher interest rates on government finance is eliminated. Debt monetization isn’t directly inflationary because deficit spending is already being removed by trade deficits, stock buybacks and dividend payments.

Debt monetization will results in a decline in the about of interest-bearing government bonds in circulation, driving up their price and lowering interest rates, unless the Fed acts by issuing bonds, with the interest paid by the Fed through money creation. There is no free lunch, using the coins simply diverts the inflationary effects of fiscal imbalance away from the real economy to the financial economy. That is, it will function like QE, eventually triggering a mighty bull market, destroying secular bear market psychology.

There goes your last protection against inflation without directly lowering Balance, which would require large tax increases on affluent and well as rich Americans and spending cuts as well, which would be difficult for Democrats considering the recent shift in the voting behavior of the wealthy toward Democrats. In the absence of such tax increases and fiscal restraint, inflation will come, and Democrats will repeat what they did sixty years ago and torpedo their dispensation.

If the Republican party fails to collapse on its own, I see no way (short of large-scale war) to permanently deal with the MAGA threat without an eventual resort to large-scale tax increases on affluent as well as rich Americans. If readers can see a way, please comment.