Political perils of economic policy

President Biden sought to create a pro-worker economy by pursuing a policy of job creation through government initiative, but it hasn't yielded political benefits.

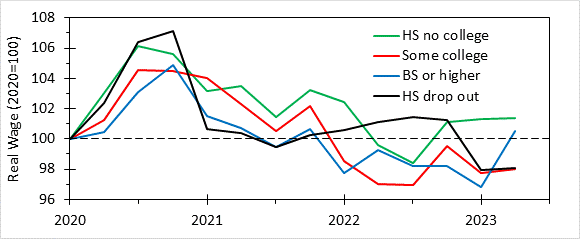

Commentators such as Paul Krugman in this New York Times article have written about how many Americans feel pessimistic about the economy, even though the economic data are good and have been for a long time. Economics writer and rabbit enthusiast Noah Smith suggests that the reason people are pessimistic about the economy is that real wages have been going down for the last couple years. Responders to Smith’s article on Substack Notes showed data indicating that lower income workers may not have seen the same decline shown by the aggregate wage series Smith cited. Looking into this, I checked out BEA data for usual weekly wages by educational level and saw that wages were down from late 2020 for all education levels, suggesting that wage growth not keeping up with inflation was a fairly widespread phenomenon (see Figure 1).

{kind=link}

Figure 1. Real wage trends for different educational levels 2020-present

The Times article acknowledged that real wages were down, but then qualified that observation by noting that this had been true under Reagan, and had not diminished his popularity. So why was it different this time? The reason seems obvious to me. After having risen steadily for forty years, real wages stopped rising after 1973. By Reagan’s re-election workers were no longer expecting economic policymakers would deliver the sort of economy that produced rising wages. As I have previously written, 1960’s Democrats had stopped supporting the New Deal order that had delivered those rising wages. By the 1980’s workers had figured out that neither party was looking out for their interests, and so politics became about other things.

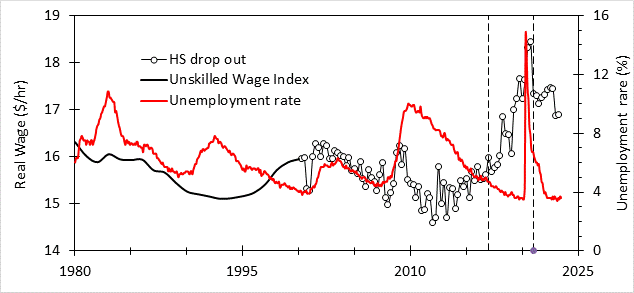

The situation today is different. Figure 2 shows a plot of real wages for high school dropouts since 2020. I use an unskilled wage index to extend this series back to 1980. The longer perspective shows that hourly wages had varied between a high of just over $16 to just under $15 over 1980-2017 period. The fluctuations followed the ups and down of the business cycle as indicated by corresponding trends in unemployment rate. That is, the same no-wage growth wage trend already present during Reagan’s first term had continued on for more than three decades.

Figure 2. Real wages and unemployment rate over 1980-present

But then something unusual happened. Real wages rose to new higher levels not previously seen after 2017. The previous high point of wages had been at the end of the 1990’s boom, itself an extraordinarily long cyclical expansion. Unemployment fell below 4% in 2000, and averaged 4% in that year, suggesting labor shortfalls were driving wages higher.

Unemployment fell below the lows responsible for the previous wage peak in 2018 and continued falling afterward, reaching a low of 3.5% just before the pandemic compared to the previous low of 3.8% in 2000. Similarly, real wages rose to a peak of $18.45, higher than the previous peak of $16.29. Since the pandemic, employment has recovered and gone to new highs, with unemployment rate reaching a new low of 3.4% in April of this year, and yet real wage at $16.89, is well below its peak before the pandemic.

President Biden, long-time, self-defined champion of the working man, has overseen tremendous employment growth, and yet what working people see is shown by Figure 2, huge gains in real wages during the Trump administration (indicated by the dashed vertical lines) and declines afterward. It is a bitter pill to swallow. He has done much to enable economic growth, and it has led to record levels of employment, but no returns to working people. This reinforces the loss of support for Democrats among working class whites. Working class people of color have non-economic reasons for supporting Democrats, and their growth in the fraction of the electorate has helped retain the viability of the Democratic party, but there is evidence of Republicans making gains among Latinos.

Democratic prospects are enhanced by the increasing derangement of the Republican party. Republicans have traditionally served the interests of the wealthy, but since a new high in income inequality and falling working incomes was recently achieved under the Biden Administration, does it make sense to continue to back this increasingly extreme party? The Republicans have always been a pro-capitalist, anti-labor party, so to try to build working class support with pro-worker policies would be to bend so much they would break. And so, they work around the edges, cultivating a sect of MAGA extremists they (or least their erstwhile leader believes) will turn the tide, hoping to ride out the storm of the Crisis.

But the working-class problem for the Democrats remains. “Lunch-bucket” Joe Biden has done pretty much all that is possible under the current Reagan disposition to and yet he remains unpopular on economics and the sort of white work class folks he came from now reject him. Sure, he’s an elite who long ago left that world, but he is also a politician who entered the business in 1972, when the New Deal order was still operative and the lunch bucket Democrat was still a real thing. It’s got to hurt.

Assuming we avoid recession, it is likely the low unemployment will result in modestly higher wages for entry-level workers., as inflation subsides, but this isn’t going to cut it for Democrats. Nobody expects Republicans to benefit anyone but the rich, but under Biden the middle 40% has seen zero factor income growth per adult, while the top 1% saw 11.9% and the top 0.01% saw a 22.4% rise. Compare to what was seen under the Trump administration: 2.7% gains for bottom 50% and middle 40%, 6.7% gain for top 1% and 0.5% loss for top 0.01%, or the Obama administration where the figures for the bottom 50% were a 2.5% gain compared to 20.5% and 21.6% for the top 1% and 0.01%. For those born after 1987, the idea that Democrats stand for working people against Republican capitalists who would exploit them is simply not borne out by the data.

In contrast, for late wave Boomers through early wave Millennials the situation was very different. The statistics show this clearly. The gain for the bottom 50% and the top 1% for the Reagan administration was, respectively, -5% and +63%, for the Clinton it was +30% and +30% and +45%, and for Bush it was -11%, and +4%. The Democratic pro-worker brand (at least compared to Republicans) remained intact while those born before the late 1980’s formed the younger half of the electorate. But as they aged, their sense of economics stopped being about themselves and became more about their kids. And has we saw above, the economic record for Democrats since the 2008 crisis has not been consistent with the idea of Democrats being the party for working people.

On the other hand, the experience of strong real wage growth during the Trump administration (denoted by vertical dashed lines in Figure 2) could become a problem for Democrats. The reason is the Trump administration did nothing that would be expected to produce real wage growth, Economic policy was the same tax cut and deregulation schtick Republicans have played since 1980. Trump did pursue some minor tariffs, which had no material impact on the trade deficit, which was actually slightly higher under Trump (2.8% of GDP) that it has been during Obama’s second term (2.7%). In contrast to Trump, Biden has made a serious effort to boost working people’s fortunes through strong job creation. The unemployment rate when Trump became president was 4.7%, and over the 37 months before the pandemic, 6.7 million jobs were created under Trump, bringing unemployment down to 3.5%. Unemployment reached 4.7% in September 2021, and in the 21 months since then, 8.4 million jobs were created under Biden, leading to an even lower unemployment rate of 3.4%. Yet stronger job growth under Biden gave falling real wages while the weaker job growth under Trump gave the opposite.

The problem for Democrats is that Bidenomics did what it was designed to do, boost economic activity and create lots of jobs, but that did not translate into rising living standards for working Americans and positive approval numbers for Biden. Readers will be quick to point out that real wages haven’t risen because of inflation. But there is no reason why one cannot have real wage growth in the face of inflation. FDR and Truman saw rising real wages despite substantial inflation during their administrations. The real problem with Bidenomics is that the modern economy does not translate economic gains into gains for workers.

The reason for this is SP culture, under which the objective of capitalism is to grow shareholders equity, not the economy. Noah Smith, in his assessment of mainstream macroeconomics notes that expectations seem to have played an important role in the rather rapid decline in inflation rate after the Fed began its tightening campaign. Expectations is the métier of financial markets, which are all about trying to predict the future returns from different investment products and investing accordingly. Under SP culture the real economy is an adjunct to the financial economy and so expectations should have a major effect on what the economy does. Sixty years ago, when the economy operated under SC culture one would expect fluctuations in non-financial economic elements such as fiscal and trade deficits and money supply growth to have more impact on how inflation works, implying that what Smith calls a hydraulic model might have worked better then than one based on expectations.

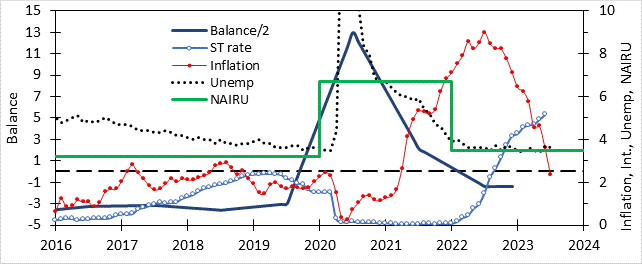

Figure 3. Balance, NAIRU, inflation, unemployment & short-term (ST) interest rate

My inflation model is of the hydraulic type and it did a pretty good job of accounting for late 1960’s through early 1980’s inflation. It managed to do a reasonable job on the recent inflation spike. Figure 3 shows how a rise in Balance due to large deficits in 2020-21 led to an increase in NAIRU, which produced inflation when unemployment fell below it. The large decline in deficit in 2021 reduced Balance and NAIRU to levels at or below unemployment rate resulting in disinflation.

Democrats failed to achieve the desired political benefits because Biden has continued to operate as a preemptive president. That is, policy must correspond to the Reagan dispensation, which favors Republicans. The only permissible economic stimulus is the neoliberal variety or supply-side sort. Policies to boost investment in infrastructure in order to create jobs is acceptable, while higher taxes on the wealthy are not. For example, Democrats passed a big spending bill that was billed as inflation-reducing, which it isn’t, inflation control was delegated to the Federal Reserve (which again is a Republican-favoring policy). There was an alternative that was not explored.

As I point out in chapter 4 of America in Crisis, a combination of high tax rates, economic stimulus and price controls gave us to the New Deal Order and the postwar era of broadly shared prosperity under SC culture. High taxes were enacted for inflation control. The way this works is through both a “hydraulic” effect (higher taxes reduce the net flow of money into the real economy via government spending) and through expectations. Consider the effect of a repeal of the 1997 and 2017 tax cuts. This would create a situation in which corporate after-tax earnings will certainly be lower next year and capital gains taken this year will be taxed more lightly that they would be next year. The immediate result of such a policy would be to send the stock market down as soon as the bill passed.

The hydraulic effect would be minimal; it is likely Balance and NAIRU would fall about as much as they actually did. Expectations are a different matter. Investors would normally expect the Fed to ride to the rescue of a falling market, but with rising inflation the Fed would not be in a position to accommodate them, choosing instead to pursue something like policy they actually did. Hence, we would expect the crashing of the cryptomarket to occur a bit earlier than it in fact did and the S&P 500 to make a much more dramatic fall. We might expect calls for hyperinflation to be replaced by calls for deflation, mass bankruptcies and the like. Expectations would shift from a “stagflation-to-soft landing” window to a “soft landing-to-depression” window, which results in a different business response to inflationary forces released by pandemic-induced shortages, increased demand, and the Russo-Ukraine war. Business might not feel so confident that massive price increases were necessarily the best way to deal with rising input costs. Some might temper price increases in order to preserve and maybe even steal market share from rivals who raised prices more aggressively in order to be better positioned for a potential deflationary recession. Such a shift in expectations as well as the Fed’s announced anti-inflation policy could result in a lower peak inflation rate and a more rapid return to the 2% level than what actually happened, allowing for the low unemployment resulting from Bidenomics to produce rising real wages and positive favorability for the President.

If Democrats wish to produce an economy that rewards work, they will need embrace tax hikes and their ability to promote SC culture. Otherwise, they yield the economic debate to the Republicans, who by pursuing their pro-wealth agenda will randomly miss (the two Bushes) and hit (Reagan & Trump) by mere chance with the same for the Democrats. In the absence of reliable pre-worker economic policy, it is questionable whether Democrats can sustain a winning coalition over the long run on the strength of their non-economic offerings alone.