Future prospects in a secular cycle crisis

Can civil strife, financial crash or other disaster be avoided?

I believe that the US is currently undergoing one of the recurrent historical crises common to all great nations and empires in history, as explained in my previous post. Previous American crises of this sort involved either internal war (Revolution, Civil War) or economic crisis (Depression). External war can play a role in these crises, for the US, WW II ended the Depression crisis, and resolved the crises in Italy, Germany and Japan in a particularly brutal way. The resolutions of the 5th century crisis in the Western Roman Empire and the 1917 end of Russian Czarist state can be described as state collapse.

We live in more enlightened times and many of these historical crisis resolutions are less relevant. We have no monarch who can abdicate, no squabbling heirs to the throne, nor is there a possibility of an external invasion. Similarly, despite idle talk it is unlikely there is going to be a repeat of the civil war. Revolution is also unlikely. As I pointed out in chapter 2 of America in Crisis, crackdowns on radicals by British authorities during the first half of the 19th Century prevented the spread of European revolutions to Britain between 1789-1848 and the deportations of thousands of immigrant radicals following the 1919 Palmer raids prevented a Leftist revolution like those in Germany, Russia, Hungary or Italy from happening in the US. These examples demonstrate the effectiveness of well-orchestrated, aggressive police tactics at forestalling revolution within Anglo polities.

I suggest in chapter 8 of America in Crisis that civil strife in America might manifest as something like the Troubles in Northern Ireland, that took the lives of over 3500 people over thirty years. During the past fifteen years the US has been more than half this death toll from mass shootings with no significant political impact. Of course, the US population is more than 160 times that of Northern Ireland. Expressed on a per capita basis, 3500 deaths over 30 years works out to a murder rate of 5.8 per 100K, six times Northern Ireland’s current murder rate of 0.9, indicating that it was a major departure for an otherwise peaceable country. Adding this death rate on to the pre-pandemic murder rate gives an American murder rate about 10-20% higher than the levels seen in the early 1990’s. This would make something like the Troubles more likely to become business as usual in an otherwise violent country.

Ten years ago, it seemed likely a repeat of the 2008 financial crisis, but this time with no bailout, might do the trick. But as I learned about Fed QE actions and then watched them spring into action at the first sign of market decline in March 2020, I realized that economic policymakers were now willing to intervene to prevent a financial crisis from happening, much less serve as a catalyst for crisis resolution as it did last cycle.

Assuming all this is true, there seems to be possibility that the current secular cycle crisis simply does not get resolved. In recent years inequality has leveled off and should remain at about the same level going forward. PSI should also level off and the current status quo continue with the two major political parties engaged in political war, but otherwise cooperating when threats to the status quo emerge. The current debt limit standoff is a good test of this idea. I believe neither party really wishes to crash financial markets, assuming this would be the response to a US default. President Biden apparently knows this and, perhaps as a riff on the US policy to not negotiate with terrorists, has chosen not to talk to House Speaker McCarthy about the issue since budgetary matters are a Congressional responsibility.

Should the Speaker decide to allow a default, and crashing markets ensue, the President can, after a suitable amount of panic has arisen, implement the platinum coin option and use the proceeds to service the country’s debt. I cannot see a win here for the Republicans; would Supreme Court by ruling this action unconstitutional send the markets crashing down again? So, I think the limit is raised at the eleventh hour, as has happened every time this issue comes up.

Assuming this is true, there seems little that can force a crisis resolution along the lines of any of the thirteen historical examples with which I am familiar. Hence in this post I consider whether the US can simply continue to remain in the crisis phase indefinitely.

Right now, the chief economic issue is inflation. According to the Balance model for inflation, the end of pandemic deficits pushed Balance down to -2.8, for which a value of 4.2% for NAIRU is obtained. Unemployment at 3.5% is still below this NAIRU and high inflation is still present. The correlation between unemployment level and the interest rate needed to raise it (see Figure 2 here) suggests interest rates above 4.5%, which were reached in February, should do the trick. Since interest rates take six months or more to work, if this argument is correct, we should see inflation subside in the fall of this year. This prediction can serve as a test of the Balance model.

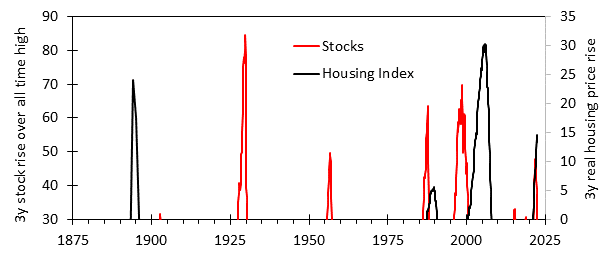

Figure 1. Speculative episodes in stocks and real estate over the past 150 years

Another potential stumbling block would a stock market crash like those in 1987 or the “tech wreck” over 2000-2. As long as asset values remain high so will the FSI (financial instability index) and the economy will remain vulnerable to such a shock. Figure 1 shows episodes of speculative price rise for the real estate and stock markets. Four episodes in which positive price appreciation in housing values in real terms are shown in the figure. The two largest spikes correspond the bubbles associated with the financial crises of 1893 and 2008. Two other episodes can be seen, one associated with the bubble associated with the 1989 savings and loan crisis, which resulted in a $132 billion bailout ($0.5 trillion in 2021) and the current housing bubble. Such episodes also occurred with stocks. The largest two were the bubbles associated with the 1929 stock market crash and the 2000 tech wreck. The next biggest spike is that associated with the 1987 stock market crash. Finally, there are two smaller spikes, one in 1957 and the other the market peak in January of last year.

Figure 1 shows that episodes of speculative frenzy that led to financial crises historically involved episodes more intense than the current one. The size of the peaks in Figure 1 matter because they can serve as a measure of the “fear of missing out” psychology that drives the use of risky financial practices by what Hyman Minsky calls Ponzi units, whose solvency depends on the continuation of the rising price trend. If this is true, then the recent stock bubble seems most similar to the 1957 bull market peak, which did not lead to any crisis.

If Fed anti-inflation policy is successful, unemployment would likely have ticked up to 4 or 5% and inflation subside to maybe 3% or even lower in a proverbial soft landing. Such a scenario means continued economic weakness through the rest of 2023. Real GDP per capita rose by 0.4% and S&P500 earnings fell by 13% over 2022, and something like that seems plausible for this year. The stock market is down only 14% from the all-time high as of the Easter weekend. Should a soft landing occur, earnings and stock prices could recover by years end. At that point, its valuation as given by the Buffet ratio (market capitalization/GDP) would be 1.85 (compared to 2.1 at the previous peak).

We can gain further insight using the stock market flow concept. This idea says that the rise in the stock market capitalization (M) can be represented as a sum of money flows into the market:

1. dM/dt = (FD D + B + I) * GDP

Here dM/dt is the rate at which M changes with time. FD is the fraction of dividends that are reinvested into the market and D, B and I represent dividends, buybacks and net investor buying as a percent of nominal GDP. Assume that nominal GDP grows at rate g and we can write:

2. GDP = G0 exp(gt) where G0 is the GDP at some reference time.

and from equation 1:

3. dM/dt = (FD D + B + I) * G0 exp(gt)

We further assume that FD, D, B, I and g are constants allowing the following expression to be written for the growth of M over time.

4. M = M0 + (FD D + B + I) * G0 /g * [exp(gt) – 1)]

Here M0 is the value of M at the same reference time when GDP was equal to G0. If we divide equation 4 by GDP (from equation 2) we get the Buffet ratio:

5. Buffet ratio = M/GDP = M0 exp(-gt) + (FD D + B + I) /g * [1 – exp(-gt)]

We are interested in the limiting behavior of this expression, that is the “equilibrium value” it tends to reach over a long period of time. This is the value for large values of t, for which the exponential functions in equation 5 will be close to zero, and we can neglect them, in which case we get:

6. Limiting Buffet ratio = (FD D + B + I)/g

In recent years B has been about 5%, D about 2% and g about 4%. Setting investor net buying (I) at zero we get a Buffet ratio between 1.25 and 1.75 for FD between 0 and 1. Since stock prices over the long run rise faster than inflation, reinvested dividends count as real returns, not nominal ones, and the current S&P 500 dividend yield of 1.5% should be compared to the real risk-free return, which right now is about 0%, but in the event of a soft landing might be around 1-2%. Since dividend investments show a similar return and have a historically validated potential for real price increases as well, a high value for FD is justified for which the equilibrium Buffet ratio with I = 0 would be about where it is now, at 1.7. This suggests that investor flows are not playing much of a role in current valuation, which is consistent with the general flat trend in the market over the better part of a year.

The investment environment after this soft landing will have changed from what it was at the previous peak in early 2022. There will be no need for interest rate reductions following a soft landing as these could easily reignite inflation. The 4.2% earnings yield for the S&P500 that gave a healthy risk premium over a near-zero risk-free return at the previous peak, provides no such premium in the new rate environment. This is no problem for dividend investors, but for growth investors, whose returns come from price rises (and face risks from price declines) the situation will not seem so appealing. With the average value for I, the equilibrium market value for the Buffet ratio is about 2.6, which suggests “room” for another 40% price rise from the previous all-time high. Against this is the historical precedent of a Buffet ratio of 1.25 after the mild pullback in 2016 and the 0.73 low after the tech wreck (the most recent bubble in Figure 1). For an assumed Buffet value of 1.85 at year’s end, there is a best-case outcome of a +0.75 rise versus worst-case outcomes of -0.6 to -1.12. This does not seem particularly bullish.

Under shareholder primacy (SP) culture the objective of economic policy can be thought of as seeking a “permanent bull market” as a goal. But this objective directly contradicts Democratic goals of increased investment in green energy projects and full employment (investment in energy infrastructure is not going into buybacks and full employment can ignite inflation resulting in higher risk-free returns). Pursuing their goals, Democrats passed a major spending bill in 2022 that could mean a higher deficit in 2023. The current push for “reshoring” may lead to a reduced trade deficit, and lack of stock market movement may incent business to reduce stock buybacks from 2022 levels. Any combination of this would result in a higher value of Balance, pushing up NAIRU and encouraging additional interest rate hikes by the Fed to fight inflation, which would be bearish.

In the past what the market did was largely the domain of investors. Businesses plied their trade, earned profits and the stock market valued them. But in the modern world of stock buybacks and QE, the decisions of noninvestors now dominate market behavior. Corporate buybacks are a bigger force than investors on average today. For example, change B to zero in equation 6 and the equilibrium Buffet ratio falls by 70% from its current level. In other words, if business executives deviate to a significant extent from their SP culture mandate, they will crash the markets and possibly produce a financial crisis. Not only that, but reducing buybacks may be inflationary since these funds will have remained in the real economy, increasing the value of Balance, and hence, NAIRU.

Should a national crisis arise requiring massive corporate investment, reducing B, we can expect a stock market crash and post-crash inflation. This means trying to avoid a crisis resolution means the nation cannot embark on a major war or other large project, which provides an additional route by which a crisis resolution might occur.