Most people define neoliberalism as the development of a more laissez faire economy after around 1980, reflecting deregulation initiatives passed around this time and afterward. Implied is that the economy before 1980 was much more regulated, that the big hand of government was stifling economic growth, and that deregulation resulted in dramatic changes to how our economy operated.

Although the 1970’s saw the passage of strong environmental and safety regulatory laws these laws have continually been updated meaning the impact of this new regulatory environment continued to expand long after 1980. Working in bulk drug manufacturing I experienced a sharp increase in environmental, safety, and FDA regulatory burdens during the 1990’s and into the 2010’s, right in the midst of the supposed era of deregulation. Higher education costs have soared over the past thirty years as colleges and universities have added large numbers of administrators to perform functions that apparently did not exist when I was in school in the 1970’s and 1980’s. Just as my industry staffed up to deal with increased regulatory requirements in the 1990’s and 2000’s, it appears higher education did as well, presumably to address different kinds of regulations than those we dealt with in pharmaceutical manufacturing. The regulatory environment post-1980 seems, if anything, greater than what came before. Some things definitely were deregulated (air travel for one) others became more regulated.

These observations suggest that the hallmark of post-1980 neoliberalism may not have been changes in regulation, per se. I see neoliberalism as the political expression of shareholder primacy (SP) economic culture. The policy at the center of this definition of neoliberalism is taxes, not regulation. Tax rates have broad effects. The 1980’s 42 percentage point cut in top income tax rate dramatically changed the business environment (as measured by E in this figure) selecting for the SP cultural variant.

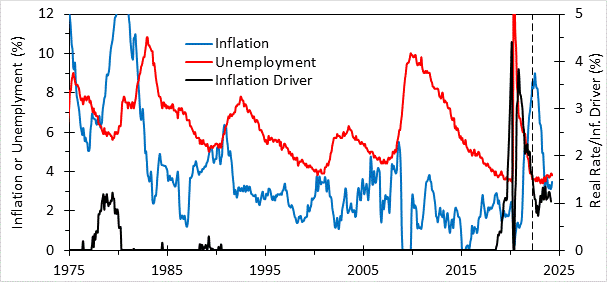

The way this selection happened has many moving parts. Tax cuts increased the federal deficit, leading the Fed to drive real interest and unemployment rates to very high levels in the early 1980’s and keep them high for the rest of the decade. This sent the inflation driver (NAIRU-unemployment rate) to zero by maintaining high levels of unemployment (see Figure 1), reducing inflation. As the economy recovered in the late 80’s, inflation driver briefly reappeared, resulting in rising inflation and a new round of interest rate hikes which sent the driver to zero once again. The inflation driver did not reappear when unemployment fell to the 4% range in the late 1990’s because fiscal surpluses kept NAIRU low.

Figure 1. Unemployment, inflation, real interest rate, and inflation driver since 1975

Low-tax, big-deficit Reaganomics had two effects on the economic environment. The first was the high deficits required high unemployment to suppress inflation. High unemployment for most of the twenty years after 1973 meant a nearly continuous labor surplus. Under these conditions labor has no market power and organized labor became impotent and never recovered. The second effect was the impact of tax cuts on executive compensation. When taxes went down it now made sense for boards to award higher monetary compensation to corporate executives as an incentive for good performance. Much of this additional compensation was in the form of stock options, which created an incentive for executives to focus on shareholder value. This focus is the core belief animating shareholder primacy (SP) economic culture.

{kind=link}

{kind=link}

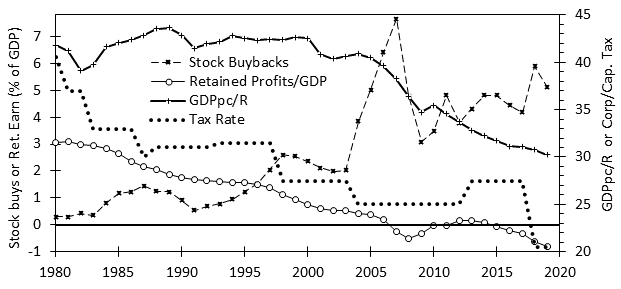

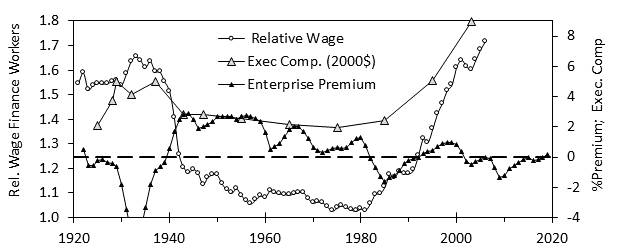

But this is not all. Stock buybacks were made fully legal by the Reagan administration in 1982. Stock buybacks provide a way for executives to directly produce shareholder value through stock market manipulation. Over time they became more popular. Stock buybacks have a deflationary impact, as well. When deficits returned after 2001, buybacks kept inflation driver zero allowing low interest rates without triggering inflation. Low interest rates and stock buybacks created conditions for strong stock market returns in the late 1990’s and since 2009. High interest rates in the 1980’s provided for strong bond returns in the 1980’s. and 1990’s. This meant that financial returns have been competitive with returns from business for much of the time since 1980. I measure the favorability of investment in business with the enterprise premium, which is the difference between the return on equity and financial returns. Enterprise premium has been lower since 1980 than it was before.

{kind=link}

{kind=link}

I define capitalism as an economic system in which capital plays the dominant role, in which capitalists seek to grow the capital they manage (i.e. maximize return on capital). Reaganomics created an economic environment in which capitalists had all the power. But what kind of capital would they grow? Real capital, defined as that which produces sales (economic output) when combined with labor and resources, or its financial representation in the stock market? Stock option compensation, legal stock buybacks, and low enterprise premium selected for the latter (i.e. shareholder primacy culture). In contrast, before 1980, when compensation was suppressed by high tax rates, stock buybacks were largely illegal, and enterprise premium was higher, the environment selected for the stakeholder capitalism (SC) cultural variant, which seeks to grow real capital, maximizing economic growth rather than market capitalization. As a result, postwar growth was unusually strong until policymakers abandoned fiscal discipline in the 1960’s and let the inflation genie out of its golden bottle.

{kind=link}

A handful of changes, chief among them tax cuts on high income individuals, led to all the things we see as characteristic of neoliberalism: rising inequality, financialization, focus on shareholder value above all else leading to outsourcing and offshoring, deficit spending, strong financial returns leading to a strong dollar and large trade deficits, and so on. The economic catechism of SP culture is supply-side economics. Biden’s “industrial policy” is just Democrat-style supply-side economics, completely consistent with SP culture and neoliberalism, according to my definition. Trump’s (and Biden’s) tariffs amount to rearranging the deck chairs on the Titanic. America will continue to decline, because the core problem, shareholder primacy culture (neoliberalism) is still ongoing. As recently as 2017, Republicans cut taxes on business, enabling larger stock buybacks, Democrats made no effect to roll these back, and candidate Trump is promising more tax cuts. Neoliberalism, according to my definition, is alive and well.

But which definition is more accurate? The conventional definition holds that the neoliberal order has ended. Apparently, this means a change in how the economy works in a direction that favors workers. My definition holds that nothing significant has changed, there will be no shift to an economy more favorable to workers. The economy will continue to work for elites and few others. This is easy to test. If neoliberalism is actually over, we should see it show up in declining inequality measures, such as top 1% income share, going forward. If it is not, inequality should stay high until top tax rates go up or the economy crashes in a future financial panic, which is yet another consequence of SP culture.

Fantastic work here. Your analyses (and I’ve only read two of your articles so far, and your comment on Ed Zitron’s Shareholder Supremacy article) strike me as right on. I am looking forwards to exploring your ideas more deeply.

I’ve just discovered you and your work and I’m gobsmacked. Really interesting! I have so many questions that I could post on all of your posts, but here’s one to start: In your account of two major elements of the Neoliberalism you describe, you say, “Low-tax, big-deficit Reaganomics had two effects on the economic environment. The first was the high deficits required high unemployment to suppress inflation. High unemployment for most of the twenty years after 1973 meant a nearly continuous labor surplus. Under these conditions labor has no market power and organized labor became impotent and never recovered. “

Later you describe Biden’s industrial investment initiatives as more “Trickle-down economics.”

But isn’t one important result of these investments that unemployment has dropped significantly? Labor power appears to be increasing, if unevenly. Isn’t this possibly a somewhat countervailing development in addressing the 40+ year bipartisan plague of neoliberalism? It has not been possible yet to address the tax code for all sorts of reasons both internal to the Dem coalition (Manchin and Sinema) and external. But is it not possible that these sorts of policies would gain traction in the next Biden administration, depending, of course, on Dem control of Congress?

So, I think you are right that shareholder value still rules the capitalist day, but is it fair to dismiss Biden’s industrial policy as a potential key piece of a post-neoliberal policy?