Effects of business cultural evolution on the stock market

I previously described my cultural evolution model for economics that explains the transition from a postwar economy of strong GDP and wage growth with low levels of inequality to the economy of today with high levels of inequality, lack of wage growth for the bottom half of the workforce, and slower growth in terms of a change in economic culture. I posit the earlier period reflected what is sometimes called stakeholder theory while the present is the product of shareholder capitalism. These two ways of thinking about business practice are formalized as two business culture archetypes: shareholder capitalism (SC) and shareholder primacy (SP). Here I explore this notion from a stock market perspective showing whether businesses culture (SC or SP) translates into different kinds of stock behavior attracting different kinds of stock investors.

Growth vs. Value Stocks

I begin with a simple stock market model in which I assume that money paid out as dividends or used for stock buybacks remains in the stock market, that is, it is re-invested in more shares of some company. So, when a company buys back stock the former owner gets cash which they then use to buy another stock. This purchase pushes up that stock’s valuation slightly so they receive slightly less capital than they sold. The former owner of the that stock then buys another stock, again getting a little less capital than they had previously. The process continues through multiple transactions until the capital changing hands shrinks to nothing and the money added by the initial purchase is consumed in incrementally driving up the price of many shares. That is, net addition of new money drives up the price of market as a whole.

This process happens every time someone buys stock using fresh money, such as the automatic investments each pay period by your 401(k), when dividends are reinvested, companies buy their own stock and individual investors use money in their money market funds to buy stocks. This is how the stock market rises over time. By buying their own stock, companies boost share prices over what would have happened in the absence of such purchases. Even though the actual recipient of the money is no longer a shareholder (having sold their shares) stock buybacks are still beneficial to the remaining shareholders through this effect on price.

The model is based on an abstract notion of a company’s stock as a share of the stock market as a whole, whose level rises due to buybacks through the mechanism described above. It is assumed that the money stays in the market and so the company’s market capitalization remains unchanged while the number of shares fall because of the company’s purchase. The company uses all of its earnings to buy stock and reinvests nothing. As a result, the company’s earnings remain unchanged, yet because there are now fewer shares, the earnings per share (EPS) rises. This company using its earnings to buy shares has a management who possess the SP culture and their stock falls into the investment category of “growth stock”.

This company is now compared to an identically-sized company having the same amount of earnings and the same market capitalization. This company’s management pursues a different model. They reinvest all of their earnings back into the business where it earns a return of 5.8%—the observed return on equity for the market as a whole over the last decade. That is, they grow the company’s earnings at a 5.8% rate. Clearly this company’s management holds the SC culture. Their stock falls into the “value” category.

I now introduce two investor archetypes: the fundamentals vs. momentum investor. A fundamentals investor analyzes their prospective investment as a business, poring over income, asset, and cash flow statements to perform valuation calculations in an effort to find good companies that are underpriced by the market. They may have read Benjamin Graham’s The Intelligent Investor and see Warren Buffet as a hero. They see themselves as investors, buying sound businesses for their attractive economics and plan to own the stock indefinitely and are often called “buy-and-hold” investors. A momentum investor is really more of a trader. They buy stocks they believe will sell at a higher price in the future and so earn their return by selling at the higher price. A momentum enthusiast might note that what one buys is a stock, not a share, and so the company’s fundamentals are irrelevant. A typical approach is to buy stocks that are currently trending upwards in price, planning to sell at a profit when the trend is ending, that is, when the momentum runs out. Such investors use what is called technical analysis to discern appropriate candidates for purchase and to identify sell points.

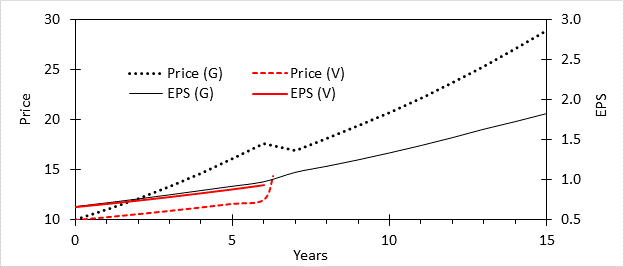

Returning to the model, I assume that rising earnings in the industry represented by these two companies attacts new investor money. Some of these investors are fundamentalists while others are momentum traders. Figure 1 compares the performance of the growth and value stock model. EPS growth for the two companies over the first six years is similar, yet the performance of the stock price is very different. The price of the growth stock has been boosted through buybacks and so shows a strongly rising trend. Consider some prospective investors coming across these stocks in year 4. Over the past four years the growth stock price has risen by 47%, reflecting a 30% increase in EPS. In contrast, the value stock has shown only a 13% price rise on a 25% rise in EPS. Momentum players see the strong EPS growth showing up as price appreciation, conclude the trend will continue, and buy the growth stock. Fundamentalists are attracted by the prospect of solid, real earnings growth (i.e. good economics) at an attractive valuation compared to the growth stock (13.8 vs. 16.4 P/E) and buy the value stock. Sooner or later the market will recognize the value here and reward them.

Figure 1. Performance of a hypothetical “growth” stock vs. a “value” stock

In year six someone does catch up with the bargain the value stock represents. The growth company makes an all-stock bid to buy the value company, offering a 20% premium to the market price. The value company shareholders accept the offer and the now larger growth company continues on as before. The value stock owners now own a “growth stock” and sell their shares to a momentum investor for a 28% return over the past two years compared to the 20% the growth investor earned over that time.

Over the 15-year period shown in the figure, the growth company management increased their share price nearly three-fold over 15 years without growing earnings by a dime. They steadily increased EPS over the same period so that the P/E for the growth stock after 15 years (15.8) was scarcely higher that its starting value of 15 (the market average). The stock was not overvalued and at risk of a decline at the end of the period. Had they attracted the sort of speculative money that buys things like crypto and high-flying tech stocks, the stock price would have been even higher and the momentum shareholder even happier with their purchase.

The way the growth stock managers did this was by using share buybacks to engineer a higher EPS and stock price, which they then used as currency to buy the earnings of the value company, after which they continued their share buyback financial engineering.

This strategy of using a high-multiple stock to acquire a lower price stock produces a what is called an accretive acquisition, that is, one in which EPS of the acquiring firm goes up as a result of the acquisition. This will happen when the P/E of the acquirer is higher than that of the acquiree multiplied by the premium. In the model the P/E for acquirer and acquiree in year six were 18 and 12, respectively. Even with the 20% premium the adjusted P/E of the latter, at 14.4, was well below that of the acquirer, and EPS for the growth stock rose from $0.98 to $1.10 as a result of the combination. While stock buybacks were not available before 1982, acquisitions of low-multiple companies by high multiple ones did happen. Conglomerates like Ling-Temco-Vought (LTV) used this strategy in the 1960’s to produce strong EPS growth and rising share price until they ran out of low-priced companies to acquire, and their lack of organic growth was revealed, upon which their stock crashed.

The negative consequences of pursuing LTV-style strategies in the 1960’s made SP-culture-following executives unattractive role models and served to discredit SP culture. By the mid-1990’s a rising level of stock buybacks made a growth through acquisition strategy feasible. CEOs operating under the SP paradigm were less managers of the firm they led, and more managers of their shareholder’s assets. Around the turn of the century, I noted that the CEO of the pharmaceutical company where I worked was referring to our slate of new products as a “portfolio.” A portfolio is a term used to refer to a collection of investments. It occurred to me that one could model a new drug as a kind of bond, which led me to think this CEO viewed his business as a collection of investments, and himself as a portfolio manager for his shareholder clients. This occurred during an eight-year period in which we went through two mergers and then we were acquired by Pfizer, the largest pharmaceutical company, after which mergers stopped as we were now too big to acquire. The focus was now on acquisitions, spinoffs and reorganization of the company in order to realize the full value of the company (that is, fetch a higher multiple on existing earnings).

{kind=link}

Manifestation of SP culture in management philosophy

I began my career in pharmaceutical manufacturing in 1988. Shortly after I started, I listened to a speech by our then CEO about his management philosophy He saw his role as serving four “constituencies;” shareholders, employees, customers and the community. Many years later I recognized what that guy was talking about was stakeholder theory (he apparently ascribed to SC culture). The subsequent executives were increasingly involved with mergers, acquisitions, spinoffs, and so forth, becoming more culturally SP. All these things became increasingly common throughout corporate America over the past 25 years.

A good example of how the shift from SC to SP culture can affect stakeholders outside of the company is illustrated by this piece by senior engineers at Boeing who warned that the excessive reductions of experienced technical staff reflecting the financial orientation of Boeing management would eventually lead to an erosion in the safety of their aircraft, which has since been confirmed by multiple problems with their new planes, leading to calls to nationalize the firm. In this case. it is customers (airliners) and the community (passengers) who were affected. A clear argument in favor of SP culture comes from a book published by GaveKal Research in 2005 about platform companies, which I wrote about it at the time:

{kind=link}

A platform company is one that no longer produces anything, but instead designs and sells things produced by others. They keep the high added-value parts of research, development, treasury and marketing in-house and farm out all the rest to external producers. By eliminating production, which ties up a lot of capital and uses a lot of resources, companies enjoy a "light balance sheet" that allows them to act swiftly on new business opportunities. Such companies often require no external financing at all to grow. When executed properly, the platform company business model provides for very high returns on invested capital. If sustainable, the platform model seems to be the way to go and GaveKal predicts Western companies will largely adopt this model in the future.

The platform model is the ultimate expression of shareholder primacy. Get rid of all the business operations that involve stakeholders and enjoy high returns to capital on the small amount of capital invested in the platform company. Back then I did not see the point of the platform company because the high return was on the small amount of capital invested in the platform company itself. What about all the other capital (e.g. retirement accounts) that need to find a return? And what are firms to do with the new capital generated by those outstanding returns? Sock it in T-bills earning a negative real return? It did not occur to me that executives would deploy the funds no longer needed for investment to generate outsized capital gains returns through stock buybacks, which is what happened.